By Vanessa Joy Matti, Maria Antoniette Lopez, Joshua Robert Arceno and Jesmar Corgos

Preface

The Philippine is the ninth largest sugar producer in the world and second largest sugar producer among the Association of Southeast Asian Nations (ASEAN) countries, after Thailand, according to Food and Agriculture Organization.1

There are atleast seventeen (17) provinces in the Philippines that are planting sugarcane. Among of these provinces are from Northern Luzon, from Visayas, and from Mindanao which occupy a land area of 422,384 hectares. Out of twenty-eight (28) sugar milling in the Philippnes, there are twelve (12) sugar milling that are operational located in Negros, Panay, Leyte, and Cebu which are producing 56% of raw sugar. Tarlac and Batangas are contributing 20% while Bukidnon contributes 24%.

It is estimated that 62,000 farmers are responsible for cultivating these farm areas giving an average yield of 57 tons per hectare. The 28 sugar mills operate at 66-percent capacity, giving an average recovery of 1.8 bags/ton cane (one bag=50 kilograms), which is low considering the sugar recovery of 2.4 bags in more efficient mills.

There are also 14 sugar refineries and four bioethanol distilleries producing 25% of the mandated ethanol market. Raw sugar production averages 2.2-2.4 million metric tons per year. Close to 700,000 Filipinos are directly employed in sugar production, and about 5-6 million more are indirectly employed, representing close to 7% of the country’s population.

The Philippines has a low sugar yield at 5.1 tons sugar per hectare. Columbia yields 2.38 times more sugar per hectare; Australia, 2.15 times; Brazil, 1.88 times; Guatemala, 1.74 times; and Thailand, 22 percent more. With respect to sugar recovery per ton of milled cane, Brazil recovers 58% more; Australia, 45%; China, 36.5%; and Thailand, 15%.2

At present, the sugar industry is threatened by at least four factors: first, the high costs of production—inputs, labor, interest rates; second, the low yield and low market price of sugar, which leads to low farm income; third, climate change, which has become more damaging in recent years; and fourth, labor shortage due to the government’s infrastructure program, the private construction boom and the 4Ps (cash transfer program), which, combined, have provided more employment options.2

In addition to the four factors mentioned-above, the group is further concerned on the effect of sugar liberalization of imports as part of free trade agreement between Association of South-East Asia Nation (“ASEAN”). Before, specific percentage of tariff was granted to the importation of sugar to the country. Tariff as discussed below is an import duties for imported products. As the sugar importation has been liberalized, what are the effects to the Philippine industry?; what are the action of the government toward sugar import liberalization? these are some of the questions that group are concernd about and these will be discussed thoroughly.

This research will be focusing on discussing the sugar tariff as part of the law is concerned and the effect of sugar import liberalization to consumers, farmers, millers, and Philippine industry.

Objectives of the Research

- Purpose of Tariff and the application to sugar

- This objective is to define and to know the purpose of the tariff under Philippine Tariff and Custome Code and the rates of Executive Order 892 known as Philippine Sugar Tariff and the free trade agreement between Associations of South-East Asia Nations.

- The Effect of Sugar Import Liberalization on consumers, farmers and millers

- This objective is to determine wether there is positive and negative effect on the consumers, farmers and millers.

- The Effect of Sugar Import Liberalization to the Philippine Industry

- This objective is to determine the effect on the export and import of sugar as part of the Philippine Industry and to determine as well the assessment made by the government to counter measure the effect of sugar import liberalization.

Research Methodology

Method of Research

The study used the interview method to obtain data on the effects of Sugar Import Liberalization to local consumers, farmers, millers and Philippine industry. The researchers prepared a complementary method of structured interviews consisting of several questions, which were distributed among representatives of each participant group.

Interviews are often used as research method in the social sciences, because they give the opportunity for a more in-depth, open discussion, and more informal, free interaction between the interviewer and the interviewee. (Potter, 2002; Winchester, 1999; Sarantakos, 2013)

Interview method was the determined to be the most applicable because it had produced subjective results and the flexible format of the interviews became a major advantage for the study. The said format contributed for a deeper explanation and understanding of the connection between sugar industry and the implementation of sugar import liberalization.

Respondents

The respondents composed of the Sugar Regulatory Administration officers, local sugarcane farmers, and consumers.

Data Gathering Procedure

The researchers personally conducted the interview to the respondents who were in the field of sugar industry. The researchers did not dwell on the quantitative information given by the respondents. The interview consisted of questions regarding the purpose and effects of sugar import liberalization to the respondents which were the objectives of the study. The interview took 15 to 20 minutes for the respondents to answer the questions. The respondents had differences of opinion on the matter which will be laid down in the next chapter. The respondents had also narrated their personal experiences in working in the sugar industry for years.

Discussion of the Research

- Purpose of Philippine Tariff and its application to Sugar

In the Philippines, there are so many laws governing sugar and other related matter concerning sugar, which are made for the benefits of the consumers, farmers and millers, for example, the revenue regulation regarding on sugar whether it considered vatable or not, the biofuel act of 2006, Republic Act No. 10659 entitle an Act Promoting and Supporting of the Competitiveness of the Sugarcand Industry and for other Purposes and etc.

However, the group focus on the Philippine tariff and the application of Philippine Sugar Tariff to Sugar products.

Philippine Tariff

Under the Tariff and Custom Code of the Philippines,tariffs are the most common kind of barrier to trade; it is a tax imposed on the import or export of goods. In general parlance, however, a tariff refers to “import duties” charged at the time goods are imported.3

Tariffs have three primary functions: to serve as a source of revenue, to protect domestic industries, and to remedy trade distortions (punitive function). The revenue function comes from the fact that the income from tariffs provides governments with a source of funding. In the past, the revenue function was indeed one of the major reasons for applying tariff.

Tariffs is also a policy tool to protect domestic industries by changing the conditions under which goods compete in such a way that competitive imports are placed at a disadvantage. In point of fact, a cursory examination of the tariff rates employed by different countries does seem to indicate that they reflect, to a considerable extent, the competitiveness of domestic industries. Punitive tariffs on the other hand may be used to remedy trade distortions resulting from measures adopted by other countries.

The Philippines uses tariff in almost all of its commodities specifically sugar. Sugar became the most important agricultural export of the Philippines between the late eighteenth century and the mid-1970s basically because of two reasons: 1) foreign exchange earned and 2) it was the basis of wealth accumulation of some Filipino elite at that time (Sugar Regulatory Administration, Retrieved 2013-05-31).

The transfer of Philippines as a colony from the Spanish to the Americans was not easy due to strong resistance from Filipino leader Emilio Aguinaldo. Soon after the fall of Aguinaldo in Palanan, Isabela, the Philippines was completely under the American rule. The Americans, unlike their predecessors, provided partial liberty to the Filipinos by preparing the latter to achieve independence and run its own government through a Commonwealth form of state. The United States treated the Philippines like one of its American states that resulted to state protection of the Philippine sugar market. Twenty-one years later in 1934, the United States enacted a quota system on sugar that remained enforced until early 70s (Master Plan for the Philippine Sugar Industry, 2010).

Since then, the Philippines had long maintained high tariffs on raw and refined sugar imports. However, upon enactment of Executive Order No. 892, it has reduced tariffs in ASEAN Trade in Goods Agreement (ATIGA) from 38 percent in 2010 to the current 5 percent, which started in 2015. This reduction in ASEAN tariffs is expected to lower Philippine sugar production and increase trade, as other ASEAN producers, particularly Thailand, have lower production costs. Despite the drop in ASEAN duties, there are still multiple administrative barriers in place to restrict imports (Sugar Regulatory Administration, Retrieved 2013-05-31).

Executive Order 892

MODIFYING THE RATES OF IMPORT DUTY ON SUGAR PRODUCTS AS PROVIDED FOR UNDER THE TARIFF AND CUSTOMS CODE OF 1978, AS AMENDED IN ORDER TO IMPLEMENT THE TARIFF REDUCTION SCHEDULE ON SUGAR PRODUCTS THROUGH THE INVOCATION OF THE PROTOCOL TO PROVIDE SPECIAL CONSIDERATION FOR RICE AND SUGAR UNDER THE COMMON EFFECTIVE PREFERENTIAL TARIFF SCHEME FOR THE ASEAN FREE TRADE AREA (CEPT-AFTA)/ASEAN TRADE IN GOODS AGREEMENT (ATIGA)

WHEREAS, the Protocol to Provide Special Consideration for Rice and Sugar (Protocol) signed during the 21st AFTA Council Meeting on 23 August 2007 in Makati, Philippines, allows an ASEAN Member State to, under exceptional cases, request for waiver from the obligations imposed under the CEPT Agreement and its related protocols with regard to rice and sugar;

WHEREAS, during the 23rd AFTA Council Meeting on 13 August 2009 in Bangkok, Thailand, the Philippines confirmed her intention to invoke the Protocol for sugar products;

WHEREAS, the Philippines submitted her official notification to the AFTA Council to invoke the Protocol in a letter dated 21 September 2009;

WHEREAS, the AFTA Council endorsed the Philippines’ request for waiver of CEPT/ATIGA commitments on sugar products through the invocation of the Protocol on 21 May 2010;

WHEREAS, the NEDA Board during its meeting on 25 May 2010 approved the tariff reduction schedule on sugar products;

WHEREAS, Section 402 of the Tariff and Customs Code of 1978 (Presidential Decree No. 1464), as amended, empowers the President of the Republic of the Philippines, upon the recommendation of the National Economic Development Authority, to modify import duties for the promotion of foreign trade;

NOW, THEREFORE, I, GLORIA MACAPAGAL-ARROYO, President of the Republic of the Philippines, pursuant to the powers vested in me under Section 402 of the Tariff and Customs Code of 1978, as amended, do hereby order:

SECTION 1. The articles specifically listed in the Annex (Philippines’ Commitment on Sugar Products through the Invocation of the Protocol to Provide Special Consideration for Rice and Sugar under the CEPT-AFTA/ATIGA) hereof, as classified under Section 104 of the Tariff and Customs Code of 1978, as amended, shall be subject to the CEPT-AFTA/ATIGA rates in accordance with the schedule indicated in Columns 4 to 9 of said Annex. The CEPT-AFTA/ATIGA rates so indicated shall be accorded to imports coming from ASEAN Member States applying CEPT concessions to the same products

SECTION 2. The tariff rates listed in the Annex are in accordance with the obligations under Articles 19 (Reduction or Elimination of Import Duties) and 21 (Issuance of Legal Enactments) of the ATIGA.

SECTION 3. From the date of effectivity of this Executive Order, all articles listed in the Annex which are entered or withdrawn from warehouses in the Philippines for consumption shall be imposed the rates of duty therein prescribed subject to compliance with the Rules of Origin as provided for in the Agreement on the CEPT Scheme for the AFTA as amended/ATIGA.

SECTION 4. Nothing in this Executive Order shall preclude the Philippines from invoking its right of recourse to all trade remedy measures provided for in its law, this Agreement and relevant international agreements as an effective device against import surges.

SECTION 5. The provisions of this Executive Order are hereby declared separable and in the event any of such provisions is declared invalid or unconstitutional, the other provisions, which are not affected thereby, remain in force and effect.

SECTION 6. All presidential issuances, administrative rules and regulations, or parts thereof, which are inconsistent with this Executive Order are hereby revoked or modified accordingly.

SECTION 7. This Executive Order shall take effect fifteen (15) days following its complete publication in the Official Gazette or in a national newspaper of general circulation.4

| Hdg. No. | AHTN Code 2007 | DESCRIPTION | Applicable CEPT Rates of Duty (%) | |||||

| 2010 | Starting 01 January | |||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||

| 17.01 | Cane or beet sugar and chemically pure sucrose, in solid form. | |||||||

| – Raw sugar not containing added flavouring or colouring matter: | ||||||||

| 1701.11.00A | Cane Sugar: In-Quota | 38 | 38 | 28 | 18 | 10 | 5 | |

| 1701.11.00B | Cane Sugar: Out-Quota | 38 | 38 | 28 | 18 | 10 | 5 | |

| 1701.12.00A | Beet Sugar: In-Quota | 38 | 38 | 28 | 18 | 10 | 5 | |

| 1701.12.00B | Beet Sugar: Out-Quota | 38 | 38 | 28 | 18 | 10 | 5 | |

| 1701.99.11 | Refined Sugar: White: | |||||||

| 1701.99.11A | – – – – – Containing over 65% by dry weight of sugar, In-Quota | 38 | 38 | 28 | 18 | 10 | 5 | |

| 1701.99.11B | – – – – – Containing over 65% by dry weight of sugar, Out-Quota | 38 | 38 | 28 | 18 | 10 | 5 |

=

As shown in the annex of the Executive Order, the tariff for sugar industry decreased from 38% to 5% in a five years. This law was used to govern the percentage of sugar tariff used in the importation of the product. The reason for the decrease of the sugar tariff was to welcome other nation product to come into the Philippines. This has great impact in the importation considering of the lowering of sugar tariff.

However, during the ASEAN meeting, there was an agreement to have free trade agreement among South-East Asia Nations which means instead of maintaining a 5% tariff, there will be a 0% tariff on sugar importation. According and confirmed by the Executive Assitant I, Office of the Sugar Board of Sugar Regulatory Administration, Frualine Grace Tamba-Acuyong, the Philippine is using the 0% tariff for sugar importation.

Free Trade Agreement of ASEAN

The Association of South-East Asian Nations is gaining considerably in importance as a trade bloc and is now the third largest in the world after the European Union and the North American Free Trade Agreement. Comprising the Asia Tigers of Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam (the ASEAN 6) with the smaller players such as Brunei, Cambodia, Laos and Myanmar, it has a combined GDP of US$2.31 trillion (2012) and is home to some 600 million people.5

Based on the briefing of ASEAN, the ASEAN bloc have largely cancelled all import and export duty taxes on items traded between them, with the exception of Cambodia, Laos, Myanmar and Vietnam, who continue to impose nominal duties on certain items. However, these too will be completely lifted as of December 31st, 2015, meaning that the entire region will be duty free from this date.5

ASEAN has entered into a number of free trade agreements with other Asian nations that are now radically altering the global sourcing and manufacturing landscape. It has a treaty with China, for example, that has effectively done away with reduced tariffs on nearly 8,000 product categories, or 90 percent of imported goods, to zero. These favourable terms have taken effect in China and in the original ASEAN members, including Brunei, Indonesia, Malaysia, the Philippines, Singapore and Thailand.5

Following the free trade agreement, the Philippine will be now accepting sugar imports at 0% tariff. This will put the country at a disadvantage considering of high cost production of sugar by millers. The liberalization of import on sugar will have a great impact in the supply of the sugar and the price of the sugar in the market considering imported sugar in the other country has lower cost and lower price. As the free flow of sugar import started, this affect eventually the miller and the farmers. Millers and farmers’ product will not be able compete on this level of pricing.

- The Effect of Sugar Import Liberalization on consumers, farmers and millers

Consumers

Sugar is one of the basic commodities commonly used at home aside from rice. Sugar is the generic name for sweet-tasting, soluble carbohydrates, many of which are used in food. Simple sugars, also called monosaccharides, include glucose, fructose, and galactose. Compound sugars, also called disaccharides or double sugars, are molecules composed of two monosaccharides joined by a glycosidic bond. Common examples are sucrose (glucose + fructose), lactose (glucose + galactose), and maltose (two molecules of glucose). In the body, compound sugars are hydrolysed into simple sugars. Table sugar, granulated sugar or regular sugar refers to sucrose, a disaccharide composed of glucose and fructose.7

According to Benjamin Diokno, the planned liberalization of sugar imports would negatively affect local producers but this would benefit a greater number of consumers. The plan to import around 200,000 metric tons of sugar seeks to address the elevated domestic inflation rate, whose upticks last year was caused by supply-side factors like a lack of supply of rice, meat and several agricultural products, he noted.8

The importation of sugar benefits consumers and hurts sugar producers. Hence, policymakers have to weigh the net gain of a policy decision — total benefits by consumers vs. total loss of sugar producers, Benjamin Diokno added.8

Prices of Sugar

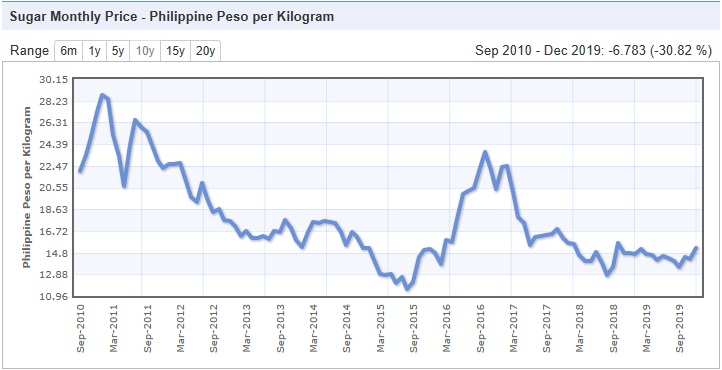

Figure 1: Sugar (world), International Sugar Agreement (ISA) daily price, raw, f.o.b. and stowed at greater Caribbean ports9

As shown in the diagram, the price of sugar in Philippine peso in the world market is very low. If the prices are too low, the cost of production of this sugar is also too low. As of September 2019, the price for sugar is PHP15 per kilogram.. The lowest price of sugar which can be be bought in the world market is PHP 10.96 per kilogram as of September 2015. While the highest price of sugar is PHP 28.23 per kilogram which can be on March 2011 from the world market.

However, it cannot be said that if the prices are too low in the world market, it will lead also to a lower price in the retail market where buyers buy the sugar product.The following are the retail market of sugar in the Philippines.

Figure 2: Retail Prices of Sugar in the Philippines based on SRA information10

Based on the graph, the retail prices does not have significant changes from December 2010 until January 2020. The prices in the market are averaging P50 to P55 for refined sugar, P45-P50 for washed sugar and P40-P46 for raw sugar.

The retail prices are higher ranging from PHP 20 to PHP 40 as compared to the prices of sugar in the world market. This means that sugar is much cheaper in the worl market. Once this cheaper sugar comes to the Philippine, the price will not probably change because there are no more tariffs that will add up to its prices. The factors that will affect the price of the sugar that comes to the Philippines will be storage and transportation fees.

Department of Agriculture (DA) Administrative Circular No. 1 (2020) imposes suggested retail prices on basic agricultural and fishery commodities in Metro Manila. The DA circular sets suggested retail prices for fully dressed chicken, raw and refined sugar, pork, fish products, garlic and red onion. The SRP for refined sugar is P50/kg and P45/kg for raw sugar (brown). This policy ensures that the retail price of sugar remains constant during the Luzon-wide lockdown or enhanced community quarantine due to COVID-19.24

There are few reasons why the world market for sugar is lower than the retail market prices. According to Chuck Kowalski in his article named World Sugar Market Versus Domestic Sugar Markets, the discrepancy in prices is due to subsidies and a tariff program that supports sugar farmers.11

In the Philippines, sugar stakeholders have blamed the lack of government support and regulation for the continued high prices of this commodity even as they face the threat of liberalization of sugar importation. Confederation of Sugar Producers Associations, Inc. (CONFED) Spokespman Raymond Montinola said that if the price of sugar in the Philippines is higher than in other countries, it is because the industry lacks government support to improve the yield of sugarcane workers as well as their production area.12

Senator Juan Miguel Zubiri said the other reason why Thailand can sell their sweetener at a very cheap price because it is only a by-product of sugarcane planting there. The Southeast Asian nation now largely uses the commodity for ethanol and power generation. “No wonder Thailand can sell their sugar very low. It is only a by-product and they just dump it like excess,” Zubiri said in a separate interview.12

The statement of Senator Zubiri was confirmed by SRA Board Member Yulo that “Thai sugar being brought to the Philippines is just excess production. The ‘A’ sugar, that’s for domestic use. Their ‘B’ sugar is just their excess production, which they export. That’s why they can bring down the cost — around PHP1,100 is the landed cost and around USD404 per metric tons. Suppose five years from now, Thailand will say, I don’t want to export to you (Philippines) anymore because I’m expanding my ethanol program. Where do we get our supply?” he said.13

Raymond Montinola, Confederation of Sugar Producers Associations, Inc. (CONFED) spokesperson, for his part, said one of the reasons why some want to have liberalization is that “they want to lower the price of sugar in the market so it would be beneficial to Filipino consumers.”13

“But if you will look at the consumption of sugar, sweeteners, 65% or 68% goes to industrial users, while institutional consumers (pastry shops), around 22% goes to them. And households consume only about 13%. So if you look at the bigger picture, who benefits the most towards liberalization? Household consumption is just around seven to eight kilograms a year per household. So who is complaining the most? It is the industrial users because they have the bigger chunk of consumption of sugar,” he noted.13

Based in the interview of some consumers, specifically those who are using sugar as commodity in the household, they are not actually bothered of the import product as long as the quality of the product is the same. As to the price, the prices of sugar increased and decreased from now and then, and they have no choice but to buy it. Their concerns as consumers are to have lower price of sugar in the market and to have a better quality product. In the market, there are variety of sugar to choose and these are refined, washed, and brown sugar. Mascuvado, a by-product of sugar, is also widely used in the market as substitute of sugar.

Basically, the consumers will still buy sugar at a retail price in the market for around PHP50 – PHP55 per kilogram. So instead of buying it low in the world market, the consumer don’t have a choice. The household consumers will not have a definite disadvantage with regard to this matter considering they are only consuming 7 to 8 kilograms a year per household. However, those industries that are using sugar in manufacturing their product like soda products, ice cream product, biscuits product, cake products, etc. have the disadvantage considering they are paying PHP50-PHP55 sugar per kilogram where in fact if they buy directly to the world market, they can buy the sugar around PHP15 per kilogram. It must have been in lesser cost which may lead to lesser price of their product as well.

Farmers

There are 17 provinces in the country that are producing sugar from sugarcane. These could entail that the are a lot of farmers and workers who are relying on the sugar industry as source of income of the family and one of these provinces is the Negros Occidental.

Sugar farming is most likely the source of income of the Filipino because it is the easiest way to earn a living. According to Benjamin Diokno, the local producers are affected by the sugar import liberalization. He, however, stressed they have been urging the Department of Trade and Industry to investigate where the problem lies because “the farmers are definitely not profiting from the high cost of sugar being sold at retail outlets. Considering the fact that 75% are small farmers, they will be affected by the lower price in the world market and the free flow of imported sugar to country.

Farmers and Workers

Figure 3. Farm Size Distribution14

Majority of sugarcane farmers are considered small farmers (farms are 5 has. or below). In CY 2016-2017, as shown in Figure 3, 85% are small farmers, 14% are cultivating 5.01 to 50.00 hectares and only 1% have 50.01 hectares and above.14

The workers for the sugar farmining are being regulated by Republic Act 6982 or the Sugar Amelioration Act of 1991.Republic Act 6982 or the Sugar Amelioration Act of 1991 was passed in order to uphold the rights of the industry workers and augment their income to improve their way living. A National Tripartite Council in the Sugar Industry known as the Sugar Tripartite Council (STC) was also established in order to ensure the effective implementation of the economic and social programs for the workers. This is being implemented by the Department of Labor and Employment, in partnership with the Sugar Regulatory Administration being a member of the council, the Sugar Industry Foundation Inc., the planters’ associations and federations, and the sugar millers and refiners. A lien of P10.00 per picul of sugar is currently implemented to fund the various welfare programs for the sugar industry workers and P13.43 per ton cane for the bioethanol workers.14

As of 2019, The industry employs 720,000 workers in 17 sugar-producing provinces and on which, about 82,000 farmers — mostly agrarian reform beneficiaries and small farmers — are dependent for livelihood.13

This means that majority of the farmers are not big planters but only small farmers. These farmers rely on sugar farming as their source of income.

Plantation Areas and Farm Productivity

Figure 4.Total Plantation Area14

The total sugarcane plantation area for crop year (CY) 2018-2019 was 409,714 hectares (has.). As shown in Figure 4, the plantation area decreased by over 8000 hectares compared to CY 2017-2018. The said decrease in the plantation areas may be accounted for by the conversion of sugarcane plantations to plantations for other crops.

Approximately 67% of the total sugarcane area in the country is situated in the Visayas Region, 19% in Mindanao and the remaining 14% in Luzon.14

Figure 5. Farm Productivity14

In terms of farm productivity (measured by the quantity of cane output per unit area, TC/Ha.), as seen in Fig.4, yield in CY 2018-2019 slightly increased compared to the 51.99 tc/ha record of the previous year.14

Basically, the farm productivity drops drastically from 2016-2017 crop year to 2018-2019 crop year. This is due to the changes in the area of the plantation,as show in figure 4,which may brough about by the fact that sugar farming is not earning income as evidenced of low millsite price for the farmers.

The farmers are also affected by the sugar import liberalization. Sugar farmers in Luzon joined the fray in putting pressure on the Department of Agriculture (DA) and the Sugar Regulatory Administration (SRA) to protect the sugar industry and prevent the planned import liberalization announced by economic managers.15

Millsite Price

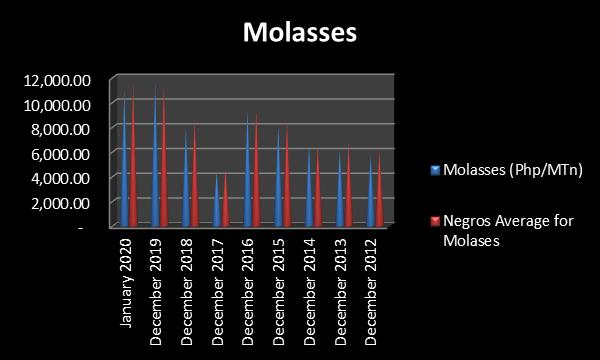

Figure 6: Millsite Price and Molasses Price16

“A” US Quota refers to sugar allocated for the export of sugar to US. “B” Domestics refers to sugar that were being used in the market. All sugar imported under this program shall be stored in an SRA-registered warehouse prior to its reclassification to “B”. “Imported sugar for replenishment shall be initially classified as “C” or Reserve sugar in their Clearances for Release of Imported Sugar.

Based on the graphs above, the price of sugar “A” is lower in 2012 as compare to the price in January 2020. The allocation of the production of sugar is smaller in “A” than to the “B” which commonly used domestic sugar. “B” is usually the price used to pay the planters or the farmers. The price of B actually ranging from P1,300 per LKG to P1,800 per LKG or the average of P1,500 per LKG for the past 8 years. This is actually a low price considering of the cost incurred by the farmers in nurturing sugarcane and growing it. The fertilizer in the market per LKG is almost the same of the lowest price of sugar per LKG.

The average monthly dealers’ price of Urea at the national level in December 2019 of P1,121.57 per sack went down by 0.4 percent from the previous month’s level. It also decreased by 0.03 percent from its level in the same period of 2018.17

Molasses are by-product of the sugar. Hence it will give an extra income to the farmers or planters. The price of Molasses was actually high in 2019. It is beneficial to the producers who have high production of sugar consider their molasses is directly proportionate to the production of their sugar.

Farmers of Philippine does not have the capacity to enhance their production through technology becauase majority are only small farmers. They rely on manpower rather on the technology that will help them enhance their production. The farm productivity decreases in crop year 2017-2018 and slightly increase in crop year 2018-2019 as shown in figure 5. However, the price received by farmers through millsite price are only averaging of PHP 1,500 for 8 years now. This millsite price cannot able to sustain the production costs of sugar farming considering of the inflation rate in the Philippines.

Based on the interview, the main concerns of the farmers as of today are the increase of prices of fertilizer, fuel and oil, and labor expenses. Maintainace of their trucks which are used in the hauling the sugarcance from farms to millsite is one of their concerns as well. They said that it is an advantage if their farm productivity increase during the year even they have not increased their planted areas. In this manner, they could earn more. If it turns out that their farm productivity decreases, they will probably incur a loss during the year. It is said that they can increase their farm productivity on the second year of cropping which means they do not plant new sugarcane crops, they allowed the old cropping after harvesting to grow. However, this will depend on how much fertilizer you put on the crop and the maintaince of the soil that will help the crop grow and it has a price to maintain the sugarcane crops healthy.

They are always expecting a higher price in the sugar considering of the cost that they shell out every year in order to nurture their sugarcane crops and to maintain their trucks and other equipment in good conditions. They said that one of the reasons of the lower prices is probably due to free flow of imported sugar to the country which causes the increase in the supply of sugar in the Philippine. Small farmers cannot dictate the price of the sugar in the market. They are actually registered in an Association that is responsible for the selling of their sugar. Once the millsite price have been set, they cannot do anything about it but to sell their products at the stated price.

Millers

In CY 2018-2019, raw sugar production slightly decreased to 2,072,351 MT.14

Figure 7. Raw Sugar Production.14

In CY 2018-2019, there were 27 operational mills and 8 sugar refineries. Seven mills are situated in Luzon, 12 in Negros Island, 3 in Panay, 2 in Eastern Visayas, and 4 in Mindanao. The mill districts have their respective Mill District Development Council (MDDC) composed of representatives from the mills, planters’ association, Philippine Sugar Research Institute and SRA created to oversee and implement programs and projects for the development of the industry.14

Figure 8. Refined Sugar Production16

The raw sugar decreased the same as the farm productivity decreased while refined sugar further decrease by 100,000 metric ton from crop year 2017-2018 to 2018-2019.

Philippine raw sugar output in CY 2019/20 declined from 2.1 million MT to 2.025 million MT,the lowest in a decade, mostly due to erratic weather conditions in sugarcane-producing areas.The contraction in sugarcane area in CY2019/20 as reported by the Sugar Regulatory Administration (SRA) also contributed to the production decline. Moreover, contacts reported unfavorable weather conditions contributing to heavier cane with lower sugar content cane, as well as continued farm labor shortage problems in sugar cane areas. MY 2019/20 sugarcane area dropped to 406,500 hectares from 410,000 hectares the previous year, with cane production that year declining to 21.8 million MT due to poor weather conditions and smaller planting area reported. Weather conditions, in particular the amount and timing of rainfall, strongly affect sugarcane output since about 80 percent of sugarcane fields are rain-fed and have no irrigation. 24

Post forecasts CY 2020/21 raw sugar production to drop to 2.0 million MT, as sugarcane areas continue to shrink due to the conversion of sugarcane lands, particularly in Luzon. Sugar producers also remain cautious about the impact of possible deregulation, as Philippine economics managers consider further trade liberalization beyond rice, such as the sugar and corn sectors. The Philippine government in 2019 ended its quantitative restrictions on rice imports by passing the Rice Tariffication Law, which eased what had become a near-decade high in food prices. The Department of Finance has mentioned sugar reform as being necessary to increase the competitiveness of Philippine food processing, particularly in comparison to its ASEAN neighbors.24

Directly, the decreased in the raw sugar production is the decreased in the farmproductivity. This means that there are factors affecting the production of millers in the recent years.

The decreased in the refined sugar production is also affected by the decreased in raw sugar production. Refined sugar productions are actually raw sugar that proceeds to another process to refine it.

Victorias Milling Company, Inc.

Victorias Milling Company, Inc., a publicly-listed company in the Philippines established in 1919, is largest producer of sugar in the country and one of the largest sugar millers and refineries in Asia. Its core business is the production of integrated raw and refined sugar and engaging in engineering services. Trading on the Philippine Stock Exchange (PSE), the company is in Victorias City, Negros Occidental, Philippines where its plant facilities are also located.18

It currently holds the biggest share of refined sugar production in the province of Negros, and in the rest of the country as well. These amount to a 23.73% and 12.63% market share, respectively. VMC’s sugar operations consist of two-mill tandems with a combined rated grinding capacity of 15,000 tonnes of cane daily. One is the VMC Walkers Mill or the “A” Mill, designed by Walkers Limited of Australia. It has a grinding capacity of 10,000 tonnes of sugarcane per day. The other one is called the “C” Mill, designed by Farell Company of Hawaii. This one has a daily grinding capacity 5,000 tonnes of sugarcane.18

Figure 9. Raw Sugar and Refined Sugar Sales of VMC(in thousand)18

During the year ended August of 2019, sales at Victorias Milling Company were 5.58 billion Philippine Pesos (US$109.30 million). This is a decrease of 15.7% versus 2018, when the company’s sales were 6.62 billion Philippine Pesos. Contributing to the drop in overall sales was the 30.7% decline in Power Generations, from 34.66 million Philippine Pesos to 24.04 million Philippine Pesos. There were also decreases in sales in Sugar Operations (down 22.0% to 4.87 billion Philippine Pesos) and Other Operations (down 4.6% to 70.27 million Philippine Pesos) . However, these declines were partially offset by the increase in sales of Distillery Operation (up 135.5% to 611.91 million Philippine Pesos).19

VMC attributed the drop in production to the El Niño episode that limited soil moisture needed for optimum growth of the sugarcane crop. This has also resulted in lower cane productivity and tonnage per hectare.20

The sugar milling business saw a 44% decline in revenues to P2.42 billion due to lower sugar net production despite the early start of refinery operations.20

The miller is only responsible of processing the sugarcane into sugar. Hence, they actually relying on the farmers for their revenues. Sale of raw sugar is recognized upon endorsement and transfer of quedans which represents ownership or title over the raw sugar. Sale of refined sugar is recognized upon approval and release of refined sugar delivery order.18

Millers depend on farmers for the production of sugarcane. Millers are only getting a percentage share of every ton milled sugarcane. Based on SRA, millers get usually 40% share of produced sugar. The farmers usually get 60% of from their total production. The percentage share sometime varies and depends on the miller of how much the miller should get from the produced sugar. In order for the miller to increase their production, they usually give incentives to sugar farmers so that these sugar farmers will have their sugarcane processed in that Miller. In Negros Occidental, there are approximately 5 millsite that can processed sugarcane to sugar and one of the biggest miller is the Victorias Milling Company located at Victorias City. Some of the millsite are located in Sagay City, Binalbagan City, EB Magalona, and La Carlota City. The competition for sugar production is very intense in Negros Occidental.

Millers have already buyers for their sugar. The price used in selling of their product is actually still based on the millsite price and is properly regulated by SRA. It is sometimes higher than the price that are being sold from the Association of farmers..

The production of raw and refined sugar is directly proportionate with the sale of Victorias Milling Company. There is decreasing trend on the production of raw and refined sugar. Although there is decrease in the revenue for raw and refined sugar of Victorias Milling Company, the Company had already have a diversed portfolio of revenue that can increase their net income during the taxable year.

Millers can be affected by the sugar import liberalization in way that their revenue is affected by the supply of sugar in the market. Their concern will probably be if their contracts for their buyer ends and the buyer does not able to continue their contract because the world market offers a lesser price of sugar than the produced sugar.

- Effect of Sugar Import Liberalization to the Philippine Industry

This research study shows numbers on the prices of sugar in the world market and retail market, sugar plantation and sugar productions of local farmers, and sugar production both raw and refind and the corresponding sales of one millers considered to be the biggest Miller in the Philippines.

Exports

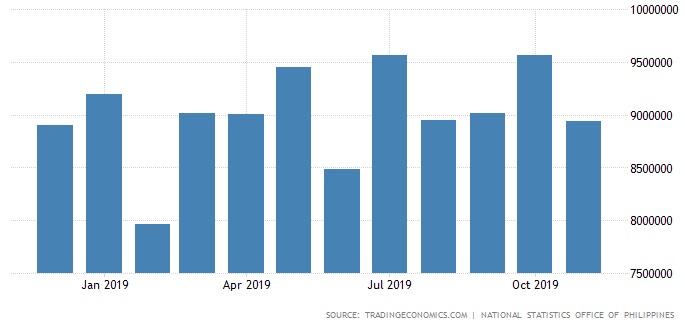

Figure 10. US exports16

The Sugar Regulatory Administration (SRA) has reduced the United States’ sugar allocation to ensure ample supply of the commodity for the domestic market, as production for the crop year 2018-2019 was projected at 2.071 million metric tons (MMT) from 2.083 MMT previously, due to the problems confronting sugar planters.21

SRA Administrator Hermenegildo Serafica, in an interview with reporters at the sidelines of the 7th Global Bioenergy Partnership at the Philippine International Convention Center (PICC) on Tuesday, said the industry could only ship 120,000 MT of sugar to the United States, a drop of 12 percent from the previous allocation of 136,201 MT, due to lower sugar output.21

The Philippines started shipping sugar to the United States in February as part of its quota under a preferential trade arrangement, which allows the country to sell sugar to the US at a premium.21

“The USDA (United States Department of Agriculture) has reallocated the shortfall of our volume to other countries so it will still be served,” Serafica said.21

Sugar planters, however, said sugar output by August 31, which is the end of the current crop year, will hit the government’s forecast of 2.071 MMT.21

Figure 11. Philippine Export 22

Exports in Philippines account for nearly a third of GDP. Major exports are: electronic products (42 percent), other manufactures (10 percent) and woodcrafts and furniture (6 percent). Philippines is also the world’s largest producer of coconut, pineapple and abaca. Philippines’s main export partners are: Japan (21 percent), the United States (15 percent), China (12 percent) and Hong Kong (8 percent).22

Exports from the Philippines fell 0.7 percent year-on-year to USD 5.59 billion in November 2019, shifting from an upwardly revised 0.3 percent growth in the previous month. Sales contracted for ignition wiring set and other wiring sets used in vehicles, aircrafts and ships (-23.7%), machinery and transport equipment (-21.7%), and electronic equipment and parts (-20.5%). In contrast, exports grew for other mineral products (74.9%), other manufactured goods (41.5%), cathodes and section of cathodes, of refined copper (36%), bananas (11.1%), metal components (3%), and chemicals (0.1%). Electronic products, the country’s top sales, rose 1.4%. By country, sales dropped to the US (-0.4%), South Korea (-16.5%), Taiwan (-17%), Netherlands (-22.1%), the ASEAN countries (-5.4%) and the EU (-8.4%) Conversely, exports were up to Japan (4.9%), Hong Kong (6.7%), China (2.9%), Singapore (4.9%), Thailand (11.9%) and Germany (8.4%).22

Based on the figure above, the export of sugar is excluded from being a major product exported from the Philippines. The main product as discussed is electronic and being followed by other manufactures. However, based on the figure from SRA, the concern is the amount of sugar being exported to US.

The largest Philippine sugar export market is the United States, as prices under the U.S. tariff rate quota system are normally higher than world market prices but lower than domesticprices. In 2019, the United States was the sole foreign market for Philippine sugar exports.24

Imports

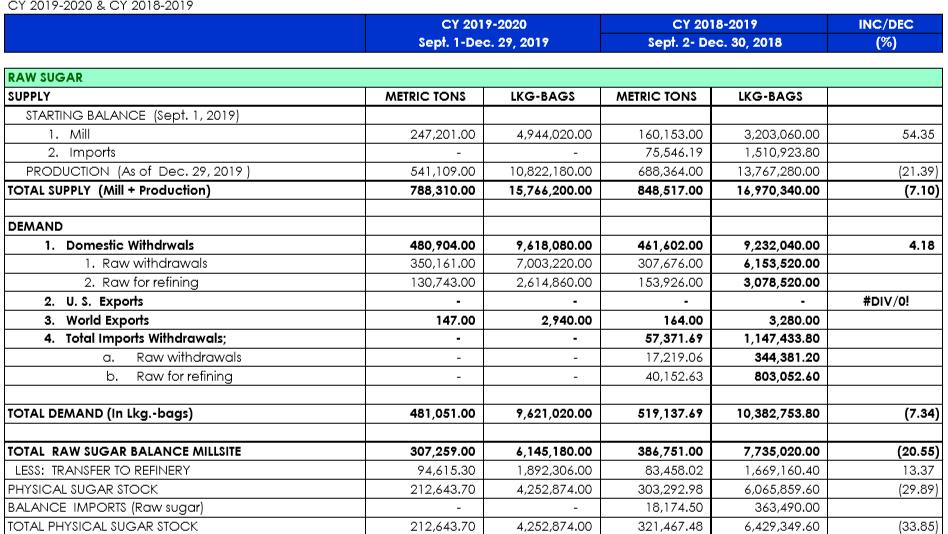

Based on the supply and demand from SRA supply and demand statistics, it can referred to the report that the importing sugar of 1.5 million LKG bags of raw sugar from abroad.16

The importation of refined sugar is a need in the country considering the Philippine is only producing lesser in a million of metric tons of refined sugar.16

Considering of the amount of sugar that the country imported to the other country, this would really affect the Philippine sugar industry. Based on the statistics above, the country is relying on importation of refined sugar which is the basic commodities in the country.

Figure 12. Philippine Imports23

Philippines major imports are: electronic products (25 percent), mineral fuels (21 percent) and transport equipment (10 percent). Philippines’s main import partners are: China (13 percent), the United States (11 percent), Japan (8 percent) and Taiwan (8 percent).23

Imports to the Philippines contracted 8 percent year-on-year to USD 8.94 billion in November 2019, the eight straight month of fall, following a 10.8 percent drop in October. Purchases dropped for mineral fuels, lubricants, related materials (-34.9%), cereals and cereal preparations (-31.1%), iron and steel (-29.8%), electronic products (-5.8%), other food and live animals (-3.7%), plastics in primary and non-primary forms (-3.4%), and industrial machinery and equipment (-3.2%). On the other hand, imports advanced for telecommunication and electrical machinery (24.8%) and miscellaneous manufactured articles (7.8%). Purchases were down from Japan (-2.1%), Thailand (-2.1%), South Korea (-45.7%), Indonesia (-0.2%), Taiwan (-7.6%), Malaysia (-5.3%), and the ASEAN countries (-5.3%). In contrast, imports increased from the US (3.6%), Hong Kong (16.1%), Singapore (5.1%), and the EU (1.4%). In addition, arrivals from China, the Philippines’s largest source of imports, rose 13.8%.

Again, sugar is not part of the major product being import in the Philippines. However, based on the SRA balances, the Philippines greatly rely on the importation of sugar specifically on the refined sugar. This is due to lesser production of raw sugar and refined sugar in the country. Hence, the sugar liberalization could affect the amount imports coming in. This sugar liberalization could ease the flow of sugar in the country as there is a greater demands than the product being produced in the country.

Governement action toward sugar import liberalization

With this, the Philippine government created a law which is the Sugar Industry Development Act (SIDA) or the Republic Act No. 10659 entitle an Act Promoting and Supporting of the Competitiveness of the Sugarcand Industry and for other Purposes and etc. to promote the competitiveness of the sugarcane industry resources and improve the income of farmers and farm workers through improved productivity, product diversification, job generation and increased efficiency of sugar mills.6

SIDA will be provided a budget of PHP2 billion pesos, during the time act was implemented, for the benefit of the farmer and millers, and the program set by the act for the sugar industry. This will be acted, institutionalized and enhanced and supported by Sugar Regulatory Administration (SRA), the Department of Agriculture (DA), the Department of Agrarian Reform (DAR), and other government agencies. Of the PHP2 billion annual fund, PHP1 billion is allocated for infrastructure for farm-to-mill roads; PHP300 million for credit; PHP100 million for scholarships: PHP300 million for block farm of the land reform beneficiaries; and PHP300 million for shared facilities program.6

The Philippines government’s counter-measure was to create a law that would promote competitiveness and efficient milling and farming for farmers and miller that produced a lower cost sugar.

Conclusion, Insights and Recommendations

Sugar industry in the Philippines is the second most protected industry next to rice. The members of the Association of South East Asian Nations (ASEAN) signed and implemented in 2010 the ASEAN Trade in Goods Agreement (ATIGA) that aims at establishing the region as a single market by 2015. Under the ATIGA, the ASEAN member countries agreed to place 99 percent of all products in the inclusion list at zero duty. The countries however agreed to maintain certain tariffs on selected items in their sensitive/highly sensitive list. The Philippines includes rice and sugar in this list. However, the Philippines, through Executive Order 892, commits to reduce gradually its sugar tariff from 38 percent in 2011 to 28 percent in 2012, to 18 percent in 2013, to 10 in 2014 and finally to 5 percent starting 2015.

The study utilized the interview method for its data gathering procedure. The said method was used to analyze the trading interactions between the Philippines and the rest of the ASEAN member countries and the rest of the world specifically foreign investors. It provided details of the industry including local sugar farmers and several household consumers and then was used to analyze the effects of the tariff on both the Philippines Sugar Industry and foreign investors.

In the analysis, sugar imports in the Philippines increased as the regional sugar tariffs are reduced. Higher sugar imports have minimal effect on sugar production, with sugar output declining marginally due to several factors such as weather, converting farm lands to industrial lands, etc. Sugar import liberazation ideally has the impact in sugar prices. Sugar prices in the world market are relatively lower from the retail market prices, though these retail prices are also regulated. The reason behind of the prices in the world market and the retail market is due to the fact that Philipines lack in government subsidies that will help sugar farmer and miller and the tariff program that supports sugar farmers. The zero tariff will eventually affect the sugar industry in a way that our sugar farmers and millers cannot anymore compete with the product introduced to us as imports from the other country considering the fact that the imported products has lower prices as compared to the production made by farmer and millers of the Philippines.

Local sugar consumers partially benefited from the reduction in sugar tariffs however the prices in the retail market are highly regulated as to not compete with the prices of the world market. Farmers were not getting any benefits from the government on how to improve their production considering of the factor that there is sugar import liberalization. The millsite per share that is given to them as the price of their farming is not enough for the expenses they have made for such farming because of the inflation of the prices of other products such fuel and fertilizers.

Currently, the government made a concrete plan that is in form of a law – Republict Act 10659 otherwised known as Sugarcane Industry Development Act – that will help the farmers and millers in the production and to help them survive with sugar import liberalization. However, the effect of such were not felt by our fellow small time farmers.

Thus, we recommend that the Philippine Government should not only provide a project that will help on improvement and enhancement of the production but must give sufficient subsidies to small time farmers and millers and in order for them to carry out their farming activities with lower cost. With that, the sugar farmers and millers who are the essential persons involved in the sugar industry will engage in sugar production more rather on selling their lot for industrial purposes. Furthermore, SRA should have the proper policy on sugar for trading and domestic prices. Considering they control on the millsite per share for the farmers, they must provide a higher prices on their productions.

Sugar import liberalization would have a minimal impact in the Philippines if the farmers, millers and traders are treated well. They are the core factor and benefactor of the sugar import liberalization however currently, this is not the situation as they suffer more than anyone else in the sugar industry. This sugar industry is one of the country’s best industries with atleast 17 provinces are planting sugarcane. However, if the government will not help these sugarcane planters or farmers, millers and traders, they will eventually suffer.

Bibliograhy

1Wikepedia – Sugar Industry of the Philippines

https://en.wikipedia.org/wiki/Sugar_industry_of_the_Philippines

2Multiple Threats to PH Sugar Industry by Teodoro C. Mendoza – Inquirer

3Tariff and Custom Duties

ntrc.gov.ph/images/Publications/guide-to-philippine-taxes-2016/tariff-and-customs-duties.pdf

4Executive Order 892 by Republic of the Philippines Tariff Commission

https://tariffcommission.gov.ph/eo-892

5Understanding ASEAN’s Free Trade Agreement by ASEAN Briefing

https://www.aseanbriefing.com/news/2014/02/13/understanding-aseans-free-trade-agreements.html

6 Republic Act No. 10659

https://www.officialgazette.gov.ph/2015/03/27/republic-act-no-10659/

7 Wikipedia – Sugar

https://en.wikipedia.org/wiki/Sugar

8Sugar import liberazation seen to benefit consumers by Joan Villanueva and Lilybeth Isun – Philippine News Agency

https://www.pna.gov.ph/articles/1060406

9Sugar Monthly Prices – Indux Mundi

Figur 1: Sugar (world), International Sugar Agreement (ISA) daily price, raw, f.o.b. and stowed at greater Caribbean ports

10 SRA – Metro Manila Prices

Figure 2: Retail Prices of Sugar in the Philippines based on SRA information

https://www.sra.gov.ph/industry-update/metro-manila-prices/

11 World Sugar Market Versus Domestic Sugar Markets by Chuck Kowalski

https://www.thebalance.com/markets-for-us-and-world-sugar-809301

12Government blamed for high sugar prices by Madelaine Miraflor

https://business.mb.com.ph/2019/03/10/govt-blamed-for-high-sugar-prices/

13SRA Board has last word on sugar importation by Lilybeth Son – Philippine News Agency

https://www.pna.gov.ph/articles/1060953

14Overview of Sugar Industry – SRA

Figure 3. Farm Size Distribution

Figure 4.Total Plantation Area

Figure 5. Farm Productivity

15Luzon farmers join call vs sugar import liberalization by Gilbert Bayoran – Philstar

16 Sugar Regulatory Administration – Sugar Statistics

Figure 6: Millsite Price and Molasses Price

Figure 8. Refined Sugar Production

Figure 10. US exports

https://www.sra.gov.ph/industry-update/sugar-statistics/

17 Update on Fertilizer Prices December 2019 – Philippine Statistics Authority

18Annual Report of Victorias Milling Company for the year ended August 2019

Figure 9. Raw Sugar and Refined Sugar Sales of VMC(in thousand)

https://www.victoriasmilling.com

19 Victorias Milling Company

https://www.corporateinformation.com/Company-Snapshot.aspx?cusip=C60881360

20Victorias Milling profit up 7% to P816 million in 10 months by Louise Maureen Simeon – Philstar

21 SRA reduces sugar export allocation to US by Lilybeth Son- Philippine News Agency

https://www.pna.gov.ph/articles/1073416

22Exports

Figure 11. Philippne Export

https://tradingeconomics.com/philippines/exports

23 Imports

Figure 12. Philippine Imports

https://tradingeconomics.com/philippines/imports

24https://www.fas.usda.gov/data/philippines-sugar-annual-4

Acknowledgement

We would like to express our deepest gratitude to the following persons who helped and guided us throughout this research. Without them, this research will not be possible.

First of all, to our Almighty God, for the knowledge that He provided us through the research.We cannot possibly think a better research without His guidance and blessing that He had given us throughout this research.

Second to our professor in Legal Research, Atty. Jocelle Batapa-Sigue, for enlightening and guiding us in our research.

Third to Ms. Frualine Grace Tamba – Acuyong, Executive Assistant I, Office of the Sugar Board, for lending your time and knowledge to our research. We are so thankful and grateful that you helped us in providing information in our research.

Fourth to our sugar farmers, Michael Francis Javellan and Jessie Corgos, for giving us the effect of sugar to you as Farmers.

Lastly to our sugar consumers, our families, for providing us information with the effect of sugar import liberalization to you.

Special thanks to our friends who helped and support us in our research. We could lose hope and we could lose track in our research but with your inspiration and support, we finally finish it.

About the Researchers

From left to right: Joshua Robert Arceno, Marie Antoniette Lopez, Vanessa Joy Matti, and Jesmar Corgos

Joshua Robert Areceno is a graduate of University of Negros Occidental Recoletos with a Bachelor of Science in Accounting Technology. He believes in a motto “Don’t succumb to the bitterness of temptation.”

Marie Antoniette Lopez is a graduate of University of Saint La Salle – Bacolod with a Bachelor of Science in Accounting Technology. She believes in a motto “Sacrifice is bitter but the bear of its fruits is sweet”.

Vanessa Joy Matti is also a graduate of University of Saint La Salle – Bacolod with a Bachelor of Science in Accountancy and a Certified Public Accountant. She believes that “failure is just a bruise not a tattoo.”

Jesmar Corgos is also a graduate of University of Saint La Salle – Bacolod with a Bachelor of Science in Accountancy and a Certified Public Accountant. He believes in a motto of Winston Churchill saying that “Never give up on something that you can’t go a day without thinking about”

All of these researchers are JD 1 students of Universtity of Saint La Salle – Bacolod, College of Law, taking up Legal Research under Atty. Jocelle Batapa-Sigue.