By Jezuel Jay G. Bayta, CPA and Naphtalie Paulle S. Betia

I. ABSTRACT

The global pandemic brought by COVID-19 evolves at unprecedented speed and scale which creates a new normal way of life. For consumers, the most immediate impact is fear, not just for personal safety but also for the economic impact. In particular, more Filipinos come to recognize and appreciate the benefits and necessity of digital finance. This thesis study concerning data privacy issue of mobile banking user and other e-wallet servicing apps in the city of Bacolod aims to achieve the following purposes: understand data privacy; safety of the customer’s data; usefulness of the application integrated in digital transaction and understanding the reason behind individuals who are still hesitant to integrate personal and business transaction digitally. In this study used to collect data from primary and secondary sources which are collected from online banking and e wallet servicing app users and bank managers through online interview and online surveys, website and other sources. The pandemic has provided substantial growth to different forms of internet banking or online banking. The use of online banking, electronic fund transfers (PESONet and InstaPay), QR code and other e wallet servicing applications for day-to-day payments such as bills payments, transportation and food deliveries have gained traction as a more convenient and safer alternative to cash transactions. As this cashless transaction continues to trend among Filipinos, this study also further discusses the Data Privacy Act 2012 or Republic Act No. 10173 which also regulates and creates a generally accepted principles and standards for personal data protection of the personal information being collected, stored, and processed. This study will show the advantages and disadvantages of integrating into digital finance which includes convenience, concern for privacy, security and etc. This study will also highlight the importance of financial and digital literacy as well as adequate consumer protection in integrating digital financial services.

II. INTRODUCTION

The meaning of the term privacy changes according to its legal context. In constitutional law, privacy means the right to make certain fundamental decisions concerning deeply personal matters free from government coercion, intimidation, or regulation. In this sense, privacy is associated with interests in autonomy, dignity, and self-determination. Under the common law, privacy generally means the right to be let alone. In this sense, privacy is associated with seclusion. Under statutory law, privacy often means the right to prevent the nonconsensual disclosure of sensitive, confidential, or discrediting information. In this sense, privacy is associated with secrecy.

The global spread of COVID-19 has generated numerous privacies, data protection, security and compliance questions. The surge of various mobile banking applications, e-wallets and other applications for cashless payments brought data privacy concerns for some users.

Under R.A. 10173 or Data Privacy Act of 2012, people whose personal information is collected, stored, and processed are called data subjects. Organizations who deal with your personal details, whereabouts, and preferences are duty bound to observe and respect an individual’s data privacy rights.

In conclusion, it is the policy of the State to protect the fundamental human right of privacy, of communication while ensuring free flow of information to promote innovation and growth. The State recognizes the vital role of information and communications technology in nation-building and its inherent obligation to ensure that personal information in information and communications systems in the government and in the private sector are secured and protected. It is well settled that the state cannot always protect its constituents thus hesitancy occurs to some individuals on how this Data Privacy Act truly protects one’s information and on to what extent does the security it provides.

III. OBJECTIVES OF THE RESEARCH

The main objective of this study is to identify data privacy issues of mobile banking users and other e-wallet servicing apps in Bacolod despite the implementation of Data Privacy Act 2012 or Republic Act No. 10173. This study focuses on the following specific objectives:

1. To perceive the advantages or disadvantages of integrating personal and business transaction digitally;

2. To identify and statistically analyze the reason behind individuals who are still hesitant to utilize mobile banking and other E-wallet servicing applications;

3. To determine the effectiveness of the Data Privacy Act 2012 or Republic Act No. 10173.

IV. RESEARCH METHODOLOGY

To meet the objectives of the research, the researchers used online platforms in order to collect data necessary in the analysis of various issues faced by existing and prospective mobile banking and other e-wallet serving apps users. Follow up online interviews were also held on some individuals with interesting responses on our survey questions and used as a secondary data source, useful for achieving the purpose of the study. Also, researchers outsourced data from different sources on the internet, such as news articles, government websites and other publications relevant to the topic. The researchers correspondingly held a collaborative discussion to evaluate the result of the study and formulate recommendations.

The researchers of this project designed an online questionnaire through google forms with answers in order to employ measurement. The questionnaires are classified into two – for user and non-user of mobile banking and other E-wallet servicing applications. All the questions employed in the questionnaire will be closed questions. This closed question is presented with a set of fixed alternatives as such respondents are expected to choose the most appropriate answer. There were opportunities for respondents to select “other” and make a comment as needed to promote a deeper response. In order to disseminate the questionnaires social media such as Gmail, Messenger and Instagram were employed. The researchers divided the questions into the following categories to cover all aspects of the research purpose: Personal information, Data group, frequency and usage of the mobile banking and other E-wallet servicing applications and concerns with Data privacy issues. Some of the questions created in each section will be discussed below.

Personal Information:

The researchers took into demographic considerations such as: sex, age group and occupation enabled the researchers assess who to survey and how to breakdown the overall survey response data into meaningful groups of respondents. Since the research was not specific to a particular gender it was important to ensure that the responses captured had an acceptable mix to eliminate bias. Additionally, the target population were young professionals who used mobile banking and E-wallet servicing applications; therefore, it was relevant to collect data on age group. The questions covered in this section were:

- What is your sex?

- In what age group do you belong?

- What is your occupation

Data Group:

- Do you use any Mobile banking or E-wallet servicing applications?

Frequency and usage of the mobile banking and other E-wallet servicing applications- User questionnaires:

This section will focus on questions specific to users of mobile banking and E-wallet servicing applications, to enable the researchers derive the users perceived benefit or limitations of the current features of the applications. This section will also provide an insight to the research issues such as frequency and usage rate the length of time of owning the app will provide details about why users use the app and explore the importance or perhaps the insignificance from the users’ perspective.

- What mobile banking application/s do you use?

- What E-wallet servicing application/s do you use?

- How do you often use the application/s?

- Mark the types of Financial transactions you do through Mobile banking and E-wallet servicing applications.

- How far is the nearest bank or remittance center from your residence?

- On a scale of 1 to 5, kindly rate your views on mobile banking and E-wallet servicing application/s.

- On a scale of 1 to 5, kindly rate the following benefits of mobile banking and E-wallet servicing application/s.

- Kindly rate how important the following reasons are for you to consider the using of mobile banking and E-wallet servicing applications.

Data privacy issues and other concerns – User questionnaires:

This section will aid the researchers in determining the existing data and security issues of current users of mobile banking and E-wallet servicing applications. Some of the questions covered within this section are:

- Kindly rate how important the following reasons are for you to consider using mobile banking and E-wallet servicing applications.

- Kindly mark what privacy and security issues you encountered from using mobile banking and E-wallet servicing applications.

- Do you read the terms and conditions before signing up for mobile banking and E-wallet servicing applications?

- Do you know that you are protected by Data Privacy Act 2012 or Republic Act No. 10173, “AN ACT PROTECTING INDIVIDUAL PERSONAL INFORMATION IN INFORMATION AND COMMUNICATIONS SYSTEMS IN THE GOVERNMENT AND THE PRIVATE SECTOR, CREATING FOR THIS PURPOSE A NATIONAL PRIVACY COMMISSION, AND FOR OTHER PURPOSES”?

- Do you recommend the usage of Mobile banking and E-wallet servicing applications?

Frequency and usage of the mobile banking and other E-wallet servicing applications- Non-User questionnaires:

This section will focus on questions specific to non-users of mobile banking and E-wallet servicing applications, to enable the researchers derive then non-users’ perception on features of the applications. This section will also provide an insight to the research issues such as familiarity towards this online financial tool:

- Kindly mark what privacy and security concerns you have for not using any mobile banking and E-wallet servicing applications.

- How far is the nearest bank or remittance center from your residence?

- On a scale of 1 to 5, kindly rate your views on mobile banking and E-wallet servicing applications.

Data privacy issues and other concerns – Non-User questionnaires:

This section will aid the researchers in determining why this particular group opt not to use the application and explore the importance or perhaps the significance from their perspective. Some of the questions covered within this section are:

- This section will aid the researchers in determining the existing data and security issues of current users of mobile banking and E-wallet servicing applications. Some of the questions covered within this section are:

- Are you familiar with the Data Privacy Act 2012 or Republic Act No. 10173, “AN ACT PROTECTING INDIVIDUAL PERSONAL INFORMATION IN INFORMATION AND COMMUNICATIONS SYSTEMS IN THE GOVERNMENT AND THE PRIVATE SECTOR, CREATING FOR THIS PURPOSE A NATIONAL PRIVACY COMMISSION, AND FOR OTHER PURPOSES”?

- Given the existence of the Data Privacy Act 2012 or Republic Act No. 10173, will you reconsider using any Financial applications in the future?

- If No, kindly rate the likelihood of the foregoing items affecting your decision in reconsidering usage of financial applications?

Response rate:

Although it was not possible to define whether most of the answers received were through social networks advertisements where a total audience of 200 were reached. Consequently, out of the 200 audience, 100 responses collected, all were valid.

V. DISCUSSION

Data Analysis:

In order to measure what is proposed in the current research, the analysis will be elaborated focusing on a specific group who are from Bacolod City which includes both users and non-users of mobile banking and E-wallet servicing applications. The information provided by the questionnaire will be analyzed considering statistical methods. The statistical analysis will be mainly presented using a descriptive approach, which describes the data collected itself, and in the current project, it will be utilized as graphical presentations of the questionnaire responses.

Part I: Personal Information

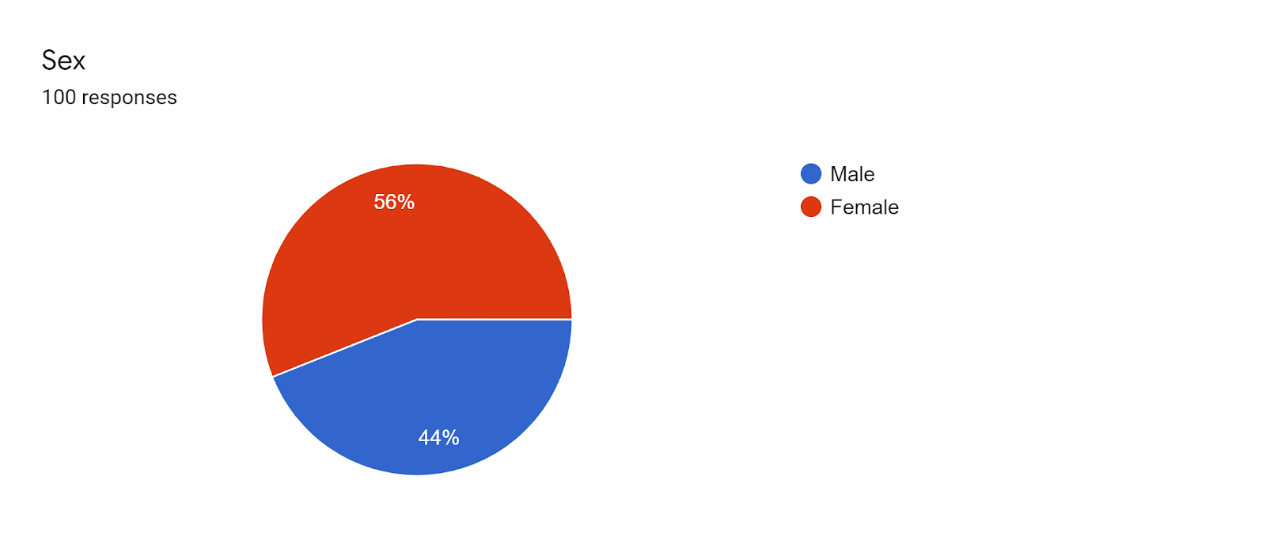

Classified by gender, 56% of the respondents were female and 44% male. As illustrated in the Figure 1 below. In addition to this Figure 2 shows that the majority of the respondents (61%) works in the private sector, followed by government workers (17%) and the remaining percentage belongs to individuals who are either unemployed, students, self-employed or freelancers.

Figure 1. Respondent based on sex

Figure 2. Respondents Occupation

As presented in Figure 3, the 21 to 30 years of age range was 81% comprising 81 respondents of the total responses. It was noted in Figure 5 that within this age group recorded the highest number of mobile banking and E-wallet servicing app users.

Figure 3. Age group

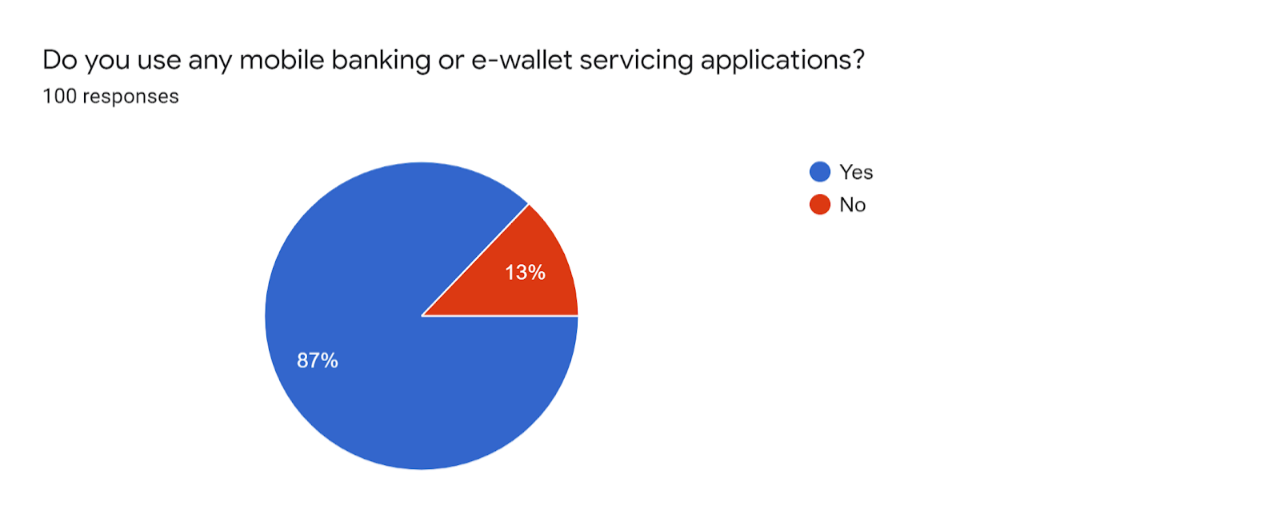

Figure 4 shows that 87% or 87 respondents of the total responses use mobile banking and E-wallet servicing applications. It was interesting to note that the majority of the high users in this case consider the use of mobile banking and E-wallet servicing applications important because of the widespread acceptance of this cashless transaction. it was noted that within the remaining 13% which comprises 13 non-users, 11 respondent shows low familiarity towards online financial applications.

Figure 4. Users of Mobile Banking and E-wallet servicing applications

Figure 5. Users of Mobile Banking and E-wallet servicing apps according to age

Part II. Mobile banking or E-wallet Servicing Applications Questionnaire – User

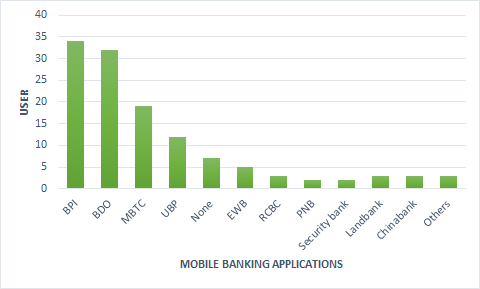

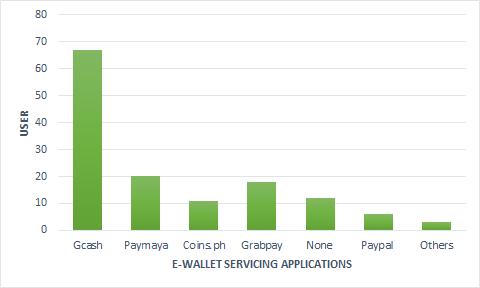

Figure 6 shows that the majority of user-respondents are using BPI’s (Bank of the Philippine Islands) online banking application. In Figure 7 below shows that on E-wallet servicing applications G-cash which is a BSP-licensed e-money issuer and remittance agent under Globe Telecom records the highest number of users.

Figure 6. Mobile Banking Applications used by respondents

Figure 7. E-wallet Servicing Applications used by respondents

Figure 8. Mobile banking and E-wallet Servicing apps frequency of usage.

In the illustrated figure 8, the highest frequency of usage is weekly. It was also noted in figure 9 below that in all frequency of usage, Fund transfer, Balance Inquiry or Bank Statement, in-store or online payment for purchases, Bills payment record the highest number of Financial transactions that the user does through mobile banking and E-wallet services applications respectively.

Figure 9. Financial Transactions incurred by respondent-users through mobile banking and E-wallet servicing applications.

In Figure 10 below, it can be considered that regardless of place of residence respondents still prefer to use mobile banking and E-wallet servicing applications for their financial transactions as represented by 24.44% of those who are 1-2 km and 29.1% of those who are 2 – 5 km away from nearest bank or remittance center. On the other hand, respondent-users who are residing more than 10 km away indicate that the use of these financial applications are cost effective and time saving.

Figure 10. Location of from place of residence to the nearest bank or remittance center.

In figure 11, it is indicated that 42 respondents maintain an average overall trust towards online financial applications and followed by 37 respondents for high, 3 for very high, 4 low and 1 respondent for very low. It is to be noted that respondent with very low overall trust indicated in privacy and security issues encountered from using mobile banking and E-wallet servicing applications is due to unsecured WIFI connections.

Trust in the technology of online banking records 43 respondents for average, 34 for high, 4 for very high and 6 low.

In security for fraud, the majority of the respondents maintain an average view with 50 respondents, 21 for high, 3 for very high, 12 low and 1 for very low.

For ease of use of online financial applications 38 respondents indicated it’s easy to utilize, 27 for average, 18 for very high and 4 for low.

It can determine in figure 11 that the majority of the respondent-users of mobile banking and E-wallet servicing applications are still skeptical as to the benefits and limitations of stated applications.

Figure 11. Respondent-users view on mobile banking and E-wallet servicing applications.

Acceptance of utilization of mobile banking and E-wallet servicing apps among respondent-users is accelerating, despite long-held industry perceptions that many are still skeptical of online security and privacy.

In a survey conducted by the researchers that polled 100 respondents, the researchers found that there is a minimal difference from average to high overall trust rating of users of this online application. It can also be noticed that only six respondents marked low trust in the technology of online banking. These six respondents marked that they only use the applications occasionally and 1 out 6 noted not to recommend the usage of this application because of lack of security of the applications. However, the majority of the respondents maintain an average trust towards the incorporation of financial and technology. 50 respondents have an average view towards security from fraud of these online applications. For the vast majority of users, the ease of use provided by online banking channels and other E-wallet applications sets a high record considering the responses of 38 respondent-users.

Figure 12. Respondent-users view on mobile banking and E-wallet servicing applications

In figure 13 below represents the following reasons indicated in the survey for respondents to consider using mobile banking and E-wallet servicing applications. With regard to lower transaction costs, the majority of the respondents (40) noted that it is important. In Time saving, security from fraud, less risk from carrying cash, safe transaction with feedback on transaction, wide acceptance of e-banking, convenient to use and user friendly apps were all indicated by the respondents to be important in considering the usage of online financial applications. There is at least 1 respondent indicated that the listed reasons are not at all important but it is to be noted that the respondent is a retiree living 1- 2 km away from the nearest bank or remittance center.

Figure 13. Respondent-users’ reasons for considering the usage of mobile banking and E-wallet servicing applications

There are various privacy and security issues encountered by user respondents as illustrated in Figure 14 below. Out of 87 responses, poor design, configuration or corrupt applications tops the list with 35 responses, it was followed by the security level of WIFI connection with 30 responses. Also, worth noting the issue concerning authentication security and the vulnerability of the application to malware.

Figure 14. Privacy and security issues encountered by respondents from using mobile banking and E-wallet servicing applications.

Application’s term and conditions elaborates the extent of services that the app provides as well as the rules and the guidelines of acceptable behavior and other useful sections to which users must agree in order to use or access the app. 65.50% of the user respondents read the terms and conditions before singing up in any mobile banking or E-wallet servicing applications as shown in Figure 15. However, 34.50% of users who were not able to read the terms and conditions reasoned out that such a document is too long and time consuming to read as illustrated in figure 16.

Figure 15: Illustration of user responses on whether or not they were able to read the terms and conditions of the financial application prior to signing up.

Figure 16: Illustration of the reasons why users were able to read the terms and conditions of the financial application prior to signing up.

In Figure 17, user respondents were asked if they are knowledgeable that they are protected by R.A. No. 10173 or the Data Privacy Act of 2012. Significantly, 73 out of 87 or 83.90% responded that they knew of R.A. 10173, contrary to 16.10% or 14 out of 87 individuals who are not knowledgeable of the protection provided by the Data Privacy Act of 2012.

Figure 17: Chart showing percentage of respondents who knew about R.A. 10173 or the Data Privacy Act of 2012.

Based on the overall assessment and experiences of the respondent-users’, we asked them whether they will recommend the usage of such app, responses are illustrated in figure 18 below. 95.50% or 83 out of 87 user respondents recommends the usage of mobile banking and e-wallet servicing applications. Only 4 responded on the opposition, with the main reason being the level of application security.

Figure 18: Chart showing percentage of respondents who recommends the usage of mobile banking or e-wallet servicing applications.

Part IV: Mobile banking or E-wallet Servicing Applications Questionnaire – Non-user Questionnaire

Data on this section is from the responses of 13 individuals who responded that they do not use any mobile banking or e-wallet servicing applications, they will be referred to as “Non-user respondents”.

We asked the privacy and security concerns of non-user respondents for not using any mobile banking and E-wallet servicing applications. Low familiarity with the financial application tops the list with 11 out 13 responses of which 63.64% belongs to 21 to 30 age group and 36.36% belongs to above 40 age group, next on the list is the doubts of non-user to try new things, then the risk of mobile malware and phishing. Other security issues were further illustrated in figure 19.

Figure 19: Chart showing various privacy and security concerns of non-users.

Researchers looked into the possibility that non-users were closely situated to a bank or any remittance center and that they prefer to transact physically in-branch. Interestingly, responses show that 66.60% of non-users, as shown in figure 20, were living more than 5 kilometers away from a nearest bank or remittance center and with only 8.3% living less than one kilometer.

Figure 20: Chart showing the distance of non-users from the nearest bank or remittance center.

In figure 20, it is indicated that 7 respondents maintain an average overall trust towards online financial applications and followed by 5 respondents for low and 1 respondent for very high. It is to be noted that respondent with very high overall trust indicated low familiarity with financial applications in privacy and security issues for not using any mobile banking and E-wallet servicing applications.

Trust in the technology of online banking records 7 respondents for average, 1 for high and 5 low.

In security, variations on the respondent answers were observed as 5 responses on the average, 4 for low, 2 for high, 1 each for very low and very high.

Figure 21. Non-user respondents’ view on mobile banking and E-wallet servicing applications.

Non-user respondents were asked if they are familiar with R.A. 10173 or the Data Privacy Act of 2012, an act protecting individual personal information in information and communications systems in the government and the private sector, creating for this purpose a national privacy commission, and for other purposes. Figure 22 depicts that 53.80% of non-users are unfamiliar with the data privacy act, whereas 46.20% shows familiarity to such law.

Figure 22: Chart showing percentage of respondents who are familiar with R.A. 10173 or the Data Privacy Act of 2012.

Significantly in figure 23, 76.90% of non-users reconsiders the usage of financial applications due to the existence of R.A. 10173 or the Data Privacy Act of 2012. However, the various reasons for non-reconsideration of the 23.10% non-users is shown in figure 24.

Figure 23: Chart showing percentage of non-user respondents’ who reconsiders the usage of financial applications due to the existence of R.A. 10173 or the Data Privacy Act of 2012.

Figure 24: Chart showing likelihood for reconsideration of non-users due to various reasons.

FINDINGS

Based on the data we gathered, we list down the advantages and disadvantages of using a mobile banking and other e-wallet servicing applications and analyze how these will affect the privacy and security issues of users.

Advantages

Throughout history, Filipinos have relied on some sort of payment system to purchase the goods or services. This payment system started with the bartering system up to the most recent, electronic payments. Traditional banks in the Philippines have made a smooth transition in incorporating finance with technology. The ability to integrate technology to provide seamless online financial services to customers that are accessible from the comfort of their home and at any time is what makes mobile banking and E-wallet servicing applications in the Philippines stand out from the rest of financial institutions. The maturing fintech sector, particularly in the payments and other financial transactions, will further boost inclusivity by facilitating easier access to basic banking services.

As stated by the researchers on their analysis with the results of the conducted online survey, it can be inferred that most of the respondents both male and female either use mobile banking or E-wallet servicing applications. Majority of these users belong to the 21-30 years old age group. It can also be noted that this age group has higher familiarity towards the availability and accessibility of these applications. These applications are largely used every week by 40.2% in completing their financial transactions. As shown in the responses, respondents noted high perceived benefits towards using mobile banking and E-wallet servicing applications. Firstly, integrating these online financial applications are cost effective. Through this advancement in technology, online transactions offer some of the lowest fees in banking. This can be done because the online banks don’t have the same level of costs as traditional banks. Second, time saving or the capacity to do financial transactions without going to the bank or ATM are also recorded with high perceived benefit by the respondents. Customers, business owners and other private individuals can do most of their financial transactions online; almost all of the transactions are possible. Adding to the advantages of using these online applications is that these transactions require only an internet connection and a computer, tablet or mobile phones. Thirdly, another advantage of these online financial applications offers 24/7 accessibility whereas individuals can make transactions anytime. As long as there is an internet connection available, Individuals can access their accounts which enables them to pay bills, fund transfer, and access records of their bank accounts. The inconvenience of long waiting lines, cut-off time, banking hours, office hours, weekends and busy schedule of customers are now minimized with the aid of online financial applications where as their financial transaction can now be done at any time of the day or night, which makes everything related to their finances a bit easier. Lastly, the lesser risk from carrying cash as individual travel is one of the listed benefits of these applications. Carrying cash makes you an easy target for criminals. Once the money is taken from your wallet and put into a criminal’s wallet, it’ll be difficult to track that cash or prove that it’s yours. As a result, there will be a relevant decrease in crime rates because there’s no tangible money to steal. Overall it cannot be denied that there are numerous benefits brought by the incorporation of financial institutions with technology. The Fintech sector made a bigger relevance especially during this time of pandemic whereas the widespread acceptance of mobile banking and E-wallet servicing applications were availed by most of the populations- from transportation up to food deliveries.

Disadvantages

As the famous saying goes “change is the only constant”, in the world where evolving technology slowly taking over the daily human task making life easier and convenient to live, included in this change is the development on conducting financial transactions specifically the introduction of mobile banking and electronic wallet servicing applications as new ways of conducting financial related transactions. This development carries numerous advantages and with this also comes various disadvantages.

The researcher cites various disadvantages of financial servicing applications based on the data collected as issues raised by respondents. Firstly, the high concern for data privacy of financial application users. As the number of users grow daily, data privacy concern also increases prompting our government to enact R.A. No. 10173 or the Data Privacy Act of 2012, an act protecting individual personal information in information and communications systems in the government and the private sector. Secondly, vulnerability of the financial applications to various fraudulent software and malicious acts such as the infusion of malwares and possible information phishing. Thus, R.A. No. 10173 or the Data Privacy Act of 2012 does not absolutely guard users against scammers and hackers but it provides safeguards in which financial application developers should adhere to ultimately protect the data of its users. Third, the technical and lengthy terms and conditions agreement of financial applications affects the level of reliability that the users pour out into the application. Terms and conditions set out the scope of services the application provides and the safety measures it adopted to protect its users, by not totally understanding the whole terms and conditions the users put themselves into a disadvantageous position. Fourth, application downtime, this is common to all applications as it requires regular updates to fix current and existing issues or to possibly introduce new features to the application. As there are times that this app downtime adversely affects users’ vital daily financial transactions. Lastly, the poor application design and configuration may cause dissatisfaction to users which may possibly lead to closure of the account, the dissatisfaction that such user experienced does not only limit up to himself as he may influence the decision of his relatives and friends in considering signing up in such application.

VI. RECOMMENDATIONS

Data security and privacy is vital for all people whether user or non-user of any mobile banking or e-wallet servicing applications. The enactment of R.A. No. 10173 or the Data Privacy Act of 2012 which authorized the creation of the National Privacy Commission strengthens the state’s policy on protecting the fundamental human right of privacy.

The weight of convenience that various financial applications provide outweighs the list of its disadvantages which was already mitigated by the government thru R.A. No. 10173. Threat of frauds and scams will always be present as technology evolves through time, users should regularly check on the updates of their applications so that their protection also increases. Thus, based on the data gathered and as what the respondents also recommended, the researchers highly recommend the usage of mobile banking and e-wallet servicing applications with caution and vigilance.

Another thing that we suggest that our Government should create a campaign to raise awareness and build overall trust in digital payments. These campaigns should not only discuss the uses and benefits but also point out the risks as well as the safety features of digital payments. Customers and business owners must also be made aware of their rights, and the importance of protecting their data and privacy.

Researchers also advocate for the modification of the terms and conditions of financial applications as the time spent in reading such lengthy and technically structured documents raise common concern among users. Users will greatly appreciate if such data policy is clear, concise and comprehensible, in this manner the users will fully understand the risk he undertakes in sharing his personal data and appreciate the protections the financial applications employ as well as the data privacy act of 2012 provides.

Most financial application users belong to the 21-30 age group, in which such are usually young working professionals which regularly have financial transactions. These individuals are a part of technology enthusiast and digitally inclined generation. They easily get fed up with usual and common features; hence, developers and application providers need to regularly improve and update the application interface and introduce novel features, included in this improvement is the review of data privacy and security that the entity provides to its users as there’s always the possibility of malware invasion and information phishing which compromises the data security of users. Frequent application feature updates are highly advisable to address privacy and security concerns. Also, introduction of user-friendly features and better in-app performance will address low familiarity and encourage non-users to sign up and avail such financial application services.

VII. BIBLIOGRAPHY

This research was conducted by First Year Juris Doctor Students of the University of St. La Salle – Bacolod under the supervision of Atty. Jocelle Batapa-Sigue.

Ms. Naphtalie Paulle S. Betia – Revenue Officer I – Bureau of Internal Revenue-RDO 077

Mr. Jezuel Jay G. Bayta, CPA – Freelance Accounting Practitioner

VIII. ACKNOWLEDGMENT

The researchers would like to express their heartfelt acknowledgement to Atty. Jocelle Batapa-Sigue for continued support and guidance throughout the course of this research.

The completion of this research would not also be possible without the help and support of our friends, classmates, co-workers, and respondents. Your participation greatly helped us in accomplishing this research.

To our ever caring, loving and supportive family, may the output of our research make you proud. Words can’t truly express how much we appreciate and love you. And finally, to our might savior and our God, your greatness is beyond comparison, your divine guidance and provisions held us through hard times and helped us complete this research. All glory belongs to you!

IX. References:

- https://www.privacy.gov.ph/know-your-rights/

- https://www.privacy.gov.ph/data-privacy-act/

- https://www.episerver.com/guides/covid-19-privacy-considerations

- https://securityintelligence.com/is-mobile-banking-safe/?fbclid=IwAR1ElmafFhxBOeg1VaWBS0O4lny1ERF8Pf-We0chIEuKIfEcq6OJE6bacME

- https://legal-dictionary.thefreedictionary.com/privacy#:~:text=In%20constitutional%20law%2C%20privacy%20means,dignity%2C%20and%20self%2Ddetermination.

- https://www.netguru.com/blog/mobile-banking-apps-security?fbclid=IwAR0efjhUxn_JVMQLo8xlXsXUP9dIANBZMVajNCBeLrluHdb8sR1C40otdoc

- https://securityintelligence.com/is-mobile-banking-safe/?fbclid=IwAR2DuYp4VManBgwYwQwk_ZUf6238G7BhibiIDZxpLrONNy9s2TboPdg4zAM

- https://www.netguru.com/blog/mobile-banking-apps-security?fbclid=IwAR0G6uIldUYjdJ5TKE9M_RMizZQo3C–yuM9pKsYq1f7DWQVVDhIjSi_zPs

- https://www.finscore.ph/how-the-data-privacy-act-of-2012-impacts-fintech-companies/?fbclid=IwAR3CT8YjT_dd-XBzCYO4J8rUnNzyhCKDckrejzZgufTZIrAFuChCiz5c-Hk

- https://www.thebalance.com/pros-and-cons-of-moving-to-a-cashless-society-4160702

- https://www.itsecurityguru.org/2017/04/26/brits-dont-trust-businesses-protect-personal-information/

- https://www.peratree.com/online-banking-philippines/

- https://www.moneymax.ph/personal-finance/articles/online-banking-pros-cons

- https://www.theasianbanker.com/updates-and-articles/how-sustainable-is-the-e-wallet-business-in-the-philippines

- https://governance.neda.gov.ph/why-the-philippines-has-been-slow-to-adopt-e-wallets/

- https://techcrunch.com/2016/06/17/the-evolution-of-the-mobile-payment/

- https://sociable.co/mobile/evolution-ewallets-history-benefits-withdrawals/

- https://builtin.com/fintech

- https://www.finscore.ph/how-the-data-privacy-act-of-2012-impacts-fintech-companies/

- https://www.bsp.gov.ph/SitePages/MediaAndResearch/SpeechesDisp.aspx?ItemId=747

- https://businessmirror.com.ph/2020/06/10/digital-payments-in-the-philippines/

- https://www.aseanbriefing.com/news/the-philippines-works-towards-national-e-payment-system/

- https://www.thebalance.com/three-advantages-of-online-banking-2385804

- https://www.thebalance.com/pros-and-cons-of-moving-to-a-cashless-society-4160702

X. GLOSSARY

- Application – is a software program or group of programs designed for end-users.

- Banking – is an industry that handles cash, credit, and other financial transactions.

- Online Banking – This offers customers almost every service traditionally available through a local branch including deposits, transfers, and online bill payments. Virtually every banking institution has some form of online banking, available both on desktop versions and through mobile apps. Online banking is also known as Internet banking or web banking.

- Mobile Banking – is the act of making financial transactions on a mobile device (cell phone, tablet, etc.). This activity can be as simple as a bank sending fraud or usage activity to a client’s cell phone or as complex as a client paying bills or sending money abroad.

- Data – the quantities, characters, or symbols on which operations are performed by a computer, being stored and transmitted in the form of electrical signals and recorded on magnetic, optical, or mechanical recording media.

- E-wallet – a digital wallet refers to an electronic device, online service, or software program that allows one party to make electronic transactions with another party bartering digital currency units for goods and services.

- Fintech – is a portmanteau of the terms “finance” and “technology” and refers to any business that uses technology to enhance or automate financial services and processes.

- Hackers – is someone who explores methods for breaching defenses and exploiting weaknesses in a computer system or network.

- Mobile – refers to a cellular device that is capable of moving or being moved.

- Privacy – is the ability of an individual or group to seclude themselves or information about themselves, and thereby express themselves selectively.

- Scammers – a person who commits fraud or participates in a dishonest scheme.

- Security – is freedom from, or resilience against, potential harm caused by others.