By Reynaldo Omandac, Jr., CPA, Jhazel Vargas Javier, CPA and Joan Pauline G. Guanzon, CPA

Introduction

It is a commitment of the current administration to make a real positive change for the Filipino people. In order to achieve such, the government initiated a Comprehensive Tax Reform Program (CTRP) which aims to accelerate poverty reduction and to address inequality by making the tax system simpler, fairer, and more efficient. The program envisions a sustainable stream of revenues to make meaningful investments in the people and infrastructure.

The CTRP is made up of six (6) packages as submitted by the Department of Finance to the Congress. In this study, the researchers will focus on the second package which is the House Bill No. 4157 entitled “Corporate Income Tax and Incentives Rationalization Act (CITIRA)”, most commonly termed as the TRAIN II.

The CITIRA seeks to lower corporate income tax rate, reform the corporate income tax system, broaden tax base by modernizing investment tax incentives, remove excessive tax exemptions and privileges given to certain industries and limit the grant of tax incentives to strategic industries and lagging regions.

The lawmakers said that the second tax package will supplement the TRAIN Law which lowered personal income tax for the middle class but imposed higher excise tax on fuels, cars, cosmetic procedures, and sweetened beverages. (Philippine Daily Inquirer, March 22, 2019)

Administration’s economic managers are supporting the measures saying that the CITIRA bill would be revenue-neutral or will not result in job losses. However, Philippine Economic Zone Authority (PEZA) Director General Charito Plaza has strongly it saying that the CITIRA bill would scare away investors due to the removal of their tax incentives.

In this study, we will find out what exactly the bill lays down, how will it affect the corporations, employment, and foreign investments, and how will this tax reform contribute to the country’s economic growth and people’s welfare

Objectives of the Study

The aim of this study is to create a side-by-side comparison of the pending House Bill No. 4157 and the existing corporate tax laws under the National Internal Revenue Code (NIRC) of 1997.

The researchers will also look into the impacts of the bill to the corporations in the Philippines with regard to revenue generation, investment attraction and creation of employment opportunities.

Lastly, the researchers will identify possible advantages and disadvantages of the bill in small to large scale industries, potential local and foreign investors, consumers, the workforce and the Philippine economy in general.

Research Methodology

In order to satisfy the objectives of the dissertation, the researchers used qualitative analysis of data gathered from different sources in the internet, such as news articles and publications of relevant firms and related agencies. Interviews were also held on randomly selected corporations in Bacolod City as secondary data source, useful for attaining the aims of the study. The researchers correspondingly held a collaborative discussion to properly draw out accurate data analysis.

Discussion

A year has already passed since the Tax Reform Acceleration and Inclusion (TRAIN) 1 took effect and mixed sentiments have been expressed by taxpayers. While the debates and analysis on TRAIN 1 approaches stillness, we are now looking to another tax reform bill.

TRAIN II proposes to gradually lower the corporate income tax rate from 30% to 20% under House Bill 4157. It also seeks to revisit the tax incentives granted to companies.

ON LOWERING THE CORPORATE INCOME TAX RATE

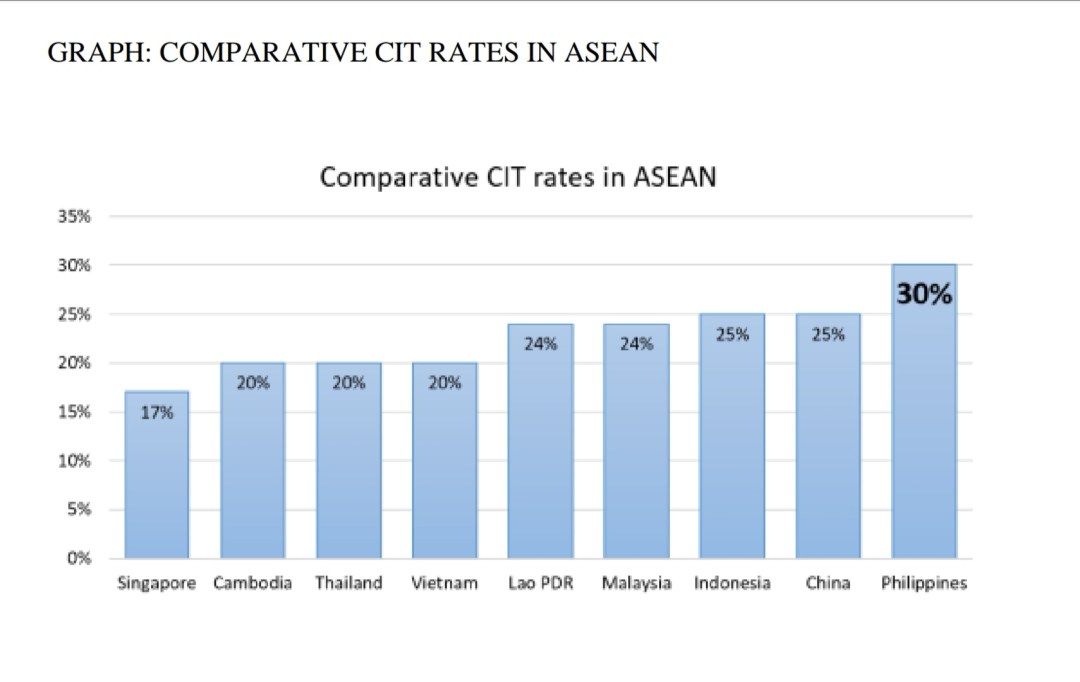

The Philippines is currently the country with the highest corporate income tax (CIT) imposed among the ASEAN countries. This results to its inability to compete with other countries with lower CIT rates. The reduction of the Philippine CIT rate will enhance its competitiveness, encouraging more multinational companies to invest.

According to the Department of Finance, the measure of lowering the CIT rate is expected to create 1.5 billion jobs because savings from a lower tax rate will allow companies to expand and create job opportunities. This action will most likely benefit micro, small and medium enterprises (MSMEs) who employ majority of Filipinos.

COMPARISON OF CITIRA AND NIRC OF 1997

In a nutshell, major differences proposed by TRAIN II against the current NIRC provisions on corporate income tax can be summarized as follows:

ANTICIPATED EFFECTS

Basically what the government wants to pursue in this tax amendment is to boost investments in the country while returning the favor to the Filipino people in terms of occupations and compensations. In consequence of a lower corporate income tax rate, domestic and resident foreign corporations acquire a higher after-tax profits — creating a possibility of a better or increased compensation package which workers can bargain over and enjoy. Further, as a result, people will obtain high purchasing power to spend on goods and services which could help improve economy. However, there are many repercussions that other departments and private companies concern about, which may have not been perceived by the government.

1. On Tax Incentives For Companies

TRAIN II discusses modernizing tax incentives for companies. The Philippines has more than 200 laws granting various types of tax incentives. In relation to this, the government is considering limits and other parameters to granting tax incentives to companies. One of the items being considered in the proposed Package 2 of TRAIN is to limit Philippine Economic Zone Authority (PEZA) incentives to a maximum of 10 years and to change the 5% tax on gross income earned to a 15% tax on net income.

This tax incentive issue is crucial, as the government has admitted that some companies and individuals will be hit by the proposed changes to the incentive system.

As an example, PEZA grants an income tax holiday (ITH) of maximum of 8 years, a “perpetual” 5% tax on gross income earned (GIE), and zero value-added tax (VAT) on local purchases, among others. With TRAIN 2 pushing its way in, a complete overhaul of the incentives regime that could reduce the tax benefits is expected.

With this overhaul, many businesses could be discouraged from investing or expanding in the Philippines. Several organizations may plan for or experience business restructuring or, at worst, may leave and close their businesses depending on the magnitude of the tax incentive reduction. Consequently, layoffs will be inevitable.

2. On Foreign investment

Right now PEZA operates nearly 400 ecozones nationwide, hosting around 3,558 firms (“locator enterprises”) in various sectors like manufacturing, agro-industry, and IT.

PEZA contends that the incentives received by its firms pale in comparison to the value they generate for our economy.

From 2015 to 2017, PEZA claims its firms got a total of P879.1 billion in investment incentives but generated over P7 trillion in export receipts, on top of other spending items.

By PEZA’s reckoning, every peso spent on incentives yields P11.4 in economic benefits.

This figure, although seemingly impressive, may be bloated because it includes not just the value of final goods (as is commonly the case) but also the value of workers’ salaries and corporate taxes.

On the other hand, the Philippines has one of the highest corporate tax rates in Southeast Asia. Currently, the corporate tax is 30%, which is applied to all net incomes from the entire tax table sources. Compared to other countries in the region, 30% is extremely steep (refer to the comparison table above). For example, the corporate tax rate in Malaysia is at 26%. This can be one of the major factors why foreign investors prefer to do business elsewhere instead of the Philippines.

Other than the country’s corporate taxes being the highest in the region, the current incentive system is also very complex and isn’t efficiently implemented. According to data, there is a huge inequity under the current system:

- Firms with no incentives pay the regular rate of 30% of net taxable income

- Firms with incentives pay between 6% and 13%

This inequity may be represented by the number of SME’s paying the regular 30% corporate tax rates, meanwhile, in the current corporate tax system, bigger businesses easily thrive due to tax incentives.

Additionally, despite giving the most generous incentives to more than 650 firms, Foreign Direct Investment still pales in comparison to neighboring regions as shown in these charts provided by the DOF.

Also, export competitiveness has been declining

INSERT GRAPH: PHILIPPINE EXPORTS

According to the report by DOF, the country’s Revenue Productivity (tax compliance of these businesses) is very low with only 12% in 2015. This is far behind Singapore’s 21%, Vietnam’s 29%, and Thailand’s 31%.

While there was a significant improvement in recent years, with this tax compliance increasing three times in 2016 compared to 2010, it is still low compared to what the emerging and developed neighbors are getting.

3. On Business Owners

While it does not have a direct effect to the consumer’s wallet, entrepreneurs and investors, on the other hand, will feel the brunt of it. Its aim is to streamline corporate taxes, taxing businesses and corporations equally. According to DOF, corporate tax rates became unequal due to the current tax incentive system. It gave tax relief to some big corporations (who aren’t necessarily causing a big impact to the economy) while many SMEs aren’t benefiting from these incentives.

Tax incentives will not be given out easily and little is known whether there will be a different tax incentive scheme.

Ultimately, businesses will be paying the same taxes across the board but not necessarily lower. Businesses who are registered under different sectors for tax incentives may have to pay higher taxes, meanwhile, local businesses not listed in sectors that are subject to tax incentives will mostly be enjoying lower taxes.

The good news is, businesses who are currently enjoying their tax holiday and incentives will be able to retain their current incentives for two years. This will grant them enough time to adjust to the new tax scheme.

Other than businesses in general, those that are registered under the following sectors will feel the brunt of it. Whether or not it’s a good impact on their business, depends on their current compliance.

4. Consumers

At this point, it isn’t exactly accurate to say that this will cause inflation but the gradual lowering down of the corporate income tax rate from 30% to 20% will most likely remove the pressure for firms to increase prices.

5. Employment

Meanwhile, in the aspect of employment, this might help the country create more jobs. That is if the said bill will be able to follow through its measures efficiently.

Supporters of the bill said the new name better reflects its objectives this tax reform package. Its goal is to create jobs by attracting the right set of investments through incentives, according to one of its proponent during a panel hearing. While TRAIN II will cut tax incentives, it will, however, grant them to businesses that will bring more jobs and provide a better contribution to the economy in the long run

It’s also a general concern that because of the lost incentives, companies will lay off employees resulting to job loss. However, the government through the Department of Finance laid down mitigating measures that counteracts such claims:

- Package 2 will lower the corporate income tax rate. This will incentivize firms to create around 1.5 million jobs

over the 10-year period.

- Package 2 will provide performance-based incentives to promote job creation.

- For every job created, the firm can deduct 150% of the compensation.

- For every training provided, the firm can deduct 200% of the training cost.

- For buying local, the firm can deduct 150% of the input cost. This will help expand the domestic supply chain.

- For investing outside NCR and poorer regions, the firm can get longer incentives and help countryside job creation.

- Package 2 will remove unnecessary incentives. Even without incentives, majority of firms will continue to operate and retain jobs because there is a profitable market or factors of production are abundant to warrant continued operation.

- A structural adjustment fund of PHP 500 million is available as a contingent fund for unforeseen job displacement. This does not mean jobs will be loss. It means we are ready to face any scenario.

- A training fund of PHP 5 billion is available to improve skills for the BPO sector to help them move up the job ladder.

- A infrastructure fund of PHP 15 billion is available to enhance competitiveness of the ecozones. This can create 15,000 jobs.

- Economy In General

While TRAIN 2 had cut down on certain incentives especially the “forever incentives,” it also gave more generous incentives to targeted recipients. It did not totally abolish incentives, which was the fear of many. It only redirected or refocused its lenses to capture the proper subjects of its generosity, keeping in mind the overall value they bring to national development. To determine the impact of incentives on economy, the DOF initially undertook a comprehensive Cost-Benefit-Analysis in 2018.

ADVANTAGES AND DISADVANTAGES BASED ON PERSPECTIVE OF CORPORATIONS

The researches have conducted a random interview on local companies here in Bacolod City with the following questions:

- Do you have an idea of the TRAIN II package? If yes, where did you hear it?

- What are your fears or expectations on the passing of the bill?

- What do you think would be TRAIN II’s general impact on your corporation? Is it advantageous or disadvantageous?

Riverside Medical Center Incorporated’s Controller, Ms. Julie Ann Christine Ko, responded accordingly:

- Yes, from the news and from the seminars I have attended.

- Since incentives are being subjected to removal, we fear that some of our suppliers who enjoy the same will pass on the monetary encumbrance to their clients. As a result, cost of sales and services will increase and we would be dealing with it with a price increase as well. We expect, ofcourse, a lower corporate tax.

- I don’t know to be honest. Basing on TRAIN 1’s impact, for individuals, I thought it would be favorable due to decrease in tax rate, but it was not because almost all prices of commodities increased.

This TRAIN 2 scheme may have the same overall impact for corporations as well. Making us believe that it would be favorable due to lowered corporate tax rate, but when we take everything into consideration, it will again have an adverse effect.

A representative from Negros Highway Tire Supply Corporation answered positively on the matter:

- Yes, TRAIN II was introduced to them through BIR Seminars and tax dialogues.

- The corporation is expecting higher return of investment since corporate income tax rate will be reduced to 20%. The decrease in the corporate tax rate would result to tax savings thereby resulting to more job opportunities, and in the long run, declaration of dividends to corporate shareholders.

- The corporation is positive about the outcome of TRAIN II. It believed that the current legislators are helping the local businesses to improve, expand and to generate more revenue. The decrease of the corporate income tax rate is a form of privilege given to them therefore, is very willing to paying their taxes correctly.

Thirdly, an interviewee from the JD Feeling Lucky, Inc., an e-games/casino station, expressed some doubts although expecting future improvement:

- The company is expecting a favorable outcome of TRAIN II which was learned by them from the local news and from seminars attended.

- The company fears that the passing of TRAIN II may revoke certain exemptions enjoyed by them under the current tax law. Since the company is exempt from business taxes, it may be denied to them under TRAIN II. The revocation from exemptions will result to the increase in their tax obligations thus causing them a lower net income.

- TRAIN II may be disadvantageous to the company because of the withdrawal of privileges and certain exemptions. But it is still hoping that the business will still grow even after the passing of TRAIN II.

Lastly, a private accountant Rosalie J. Labanero, CPA, shared her views on the topic:

- Yes, TRAIN II was explained by the BIR Tax Seminars and annual tax dialogue.

- She expects that the reform would be very beneficial to businesses especially home-grown companies to attract future employments. Moreover, the decrease in the corporate income tax would challenge the corporation to contribute more for the government through paying their correct taxes.

- TRAIN II overall impact would be friendly to corporations just like the TRAIN I of the current administration. It is expected from them to take active involvement in giving back to the community through their corporate social responsibility because the legislators favored them through the decrease in their CIT.

Lastly, Rosalie feared that since there is a decrease in the CIT, there would be an insufficiency on the collection of the BIR to achieve fiscal adequacy of taxation. This would result to cancellation of privileges and exemptions of certain taxpayers.

UNIVERSITY of Asia and the Pacific (UA&P) School of Economics Dean Cid Terosa said that just like any policy, the succeeding tax packages will have negative effects. However, these will only be for the short term.

“I believe, in the short run, negative effects will prompt adaptations and adjustments among Filipinos,” Terosa said. “In the long run, and assuming, greater efficiency in tax administration, collection, and use, we will be better off.”

Unionbank Chief Economist Ruben Carlo Asuncion believes there will be winners and losers in the tax reform packages. But the national government must ensure that everything is done transparently, especially in the rationalization of tax incentives.

Asuncion said that one of the tax reforms that will have the biggest impact on the lives of Filipinos is the Citira, but claimed it will help level the playing field for businesses.

This will particularly have an impact on micro, small and medium enterprises (MSMEs) because, Asuncion said, they will benefit from lower corporate income taxes. Due to their number, the MSMEs are the country’s largest taxpayers.

“However, Congress and government must be able to protect current wins in the employment space, careful to protect its wins,” Asuncion said. “More and targeted investments should be encouraged and not the other way around.”

Conclusion

TRAIN II projects necessary reforms that will allow us to course competitively with our neighboring countries and that are agreeably beneficial to domestic corporations, specifically the MSMEs. However, there will be transitionary risks that companies in this country will immediately face. The policy-makers should make sure that reasonable compromise and transitionary measures will be made to avoid excessive short-run costs for the long-run benefits.

Nevertheless, the implementation could be another big concern. TRAIN II incorporated the whole incentives law in the Tax Code, thereby placing it within the exclusive forecourt of the Bureau of the Internal Revenue. The challenge for our government is to prevent the possible negative impact of the proposed changes on granting tax incentives. We trust that the government’s economic advisors will fully evaluate the pros and cons of shaking the tax incentives status quo.

While the tax incentives are being analyzed, our government should think of other ways to keep investors or companies engaged in the Philippine economy.

We already have TRAIN I and TRAIN II is fast approaching. We don’t know how the other TRAIN packages will develop. Let’s hope that all these tax reforms would contribute to our country’s economic growth and to the people’s welfare.

About the Researchers:

This research is completed by Juris Doctor Students of the University of St. La Salle – Bacolod. They chose this title in line with their professions – Certified Public Accountants.

Reynaldo Omandac, Jr., CPA – Revenue Officer II of the Bureau of Internal Revenue, Revenue District Office 077.

Jhazel Vargas Javier, CPA – Financial Analyst at Riverside Medical Center, Inc.

Joan Pauline G. Guanzon, CPA – Freelance Accounting Practitioner

SOURCES:

https://www.pwc.com/ph/en/tax-alerts/assets/2019/pwc-ph-tax-alert-CITIRA.pdf

https://www.imoney.ph/articles/duterte-train-law-stage-2/

All Rights Reserved. Philippines 2019.