By Joshua R. Fuentesfina, JD 1 and Donna Lerma Janica A. Paco, JD 1

What is the TRAIN law?

REPUBLIC ACT No. 10963 more popularly known as the Tax Reform for Acceleration and Inclusion (TRAIN) Program is the first package of the Comprehensive Tax Reform Program (CTRP) that took effect on January 1, 2018, under the Duterte Administration.

How and why TRAIN law was created

House Bill No. 4774 was filed before the House of Representatives on January 17, 2017. On May 31, 2017, just before the 17th Congress adjourned its first regular session, the bill passed the final reading with 246 voting for and 9 against the bill. Duterte’s certification of the TRAIN as “urgent” allowed the bill to pass the second reading on November 28, 2017. Within the same day, the Senate bill passed the third and final reading with 17 senators voting for the bill. Finally, it was signed by President Rodrigo Duterte on December 19, 2017 and took effect on January 1 the following year.

According to the National Tax Research Center under the Department of Finance:

R.A. No. 10963 aimed to make the Philippine Tax System simpler, fairer, and more efficient to promote investments, create jobs and reduce poverty and to raise revenues that will fund the President’s (Duterte) Build, Build, Build Project.

Source: https://ntrc.gov.ph/images/train/Tax-Changes-You-Need-to-Know-under-RA-10963.pdf

Under R.A. No. 10963 were several provisions that amended the National Internal Revenue Code of 1997 on personal income taxation, passive income for both individuals and corporations, estate tax, donor’s tax, value added tax, excise tax, documentary stamp tax, and tax administration, among others. It likewise introduced new taxes on luxury products such as cosmetic and sugar-sweetened beverages (soft-drinks).

In this Legal Research Paper, we will discuss the salient points and effectiveness of R.A. No. 10963. In the same manner, we will explain the importance of the law and how it had affected our economy.

INCOME TAX

Under the Old tax Schedule for Compensation Income Earners & Self-employed and Professionals

Under the New tax Schedule that took effect on January 1, 2018, for Compensation Income Earners

For Self-employed and Professionals

For mixed Income Earners

R.A. No. 10963 exempts any person who has an annual income below P 250,000. According to surveys conducted in 2018, about P 17.7 million Filipinos earn less than P 140,000 annually and about P 40 million earn from P 140,000 to P 280,000. This means that 57 million or about half of the population can benefit from the tax exemption. The tax reform also alleviates 31 million Filipinos from poverty who earn between P 280,000 to P 560,000 annually. The new Tax system also made the rich taxpayers contribute even more. In addition, the new tax initiative allows anyone whose income exceeds P 3,000,000 to choose what tax rate they desire.

Furthermore, the new schedule eliminated the provision for deduction of basic personal and additional exemptions, as well as premiums paid on health and/or hospitalization insurance. Instead, the first P250,000 out of the total annual taxable income of a taxpayer will be exempt from Income Tax. The shift from a conditional type of availment of the deduction to a fixed and standard mode allowed more Filipinos to be benefited by the change. A compensation earner who is still single and has no dependents can avail the same privilege as that of a married employee with four dependents. Both are qualified to avail for the P250,000 exemption.

EXCISE TAX

Another important change that has produced a great impact to Filipinos is the increase in Excise tax rates in some luxury and essential products.

Excise Tax on Automobiles

Under the old tax schedule

Under the new tax schedule

Under the TRAIN Law, the purchase of Automobiles became more expensive. A person who bought a P1,000,000 car in 2018 would have saved about P8,000 if he bought the car in the same price in 2017.

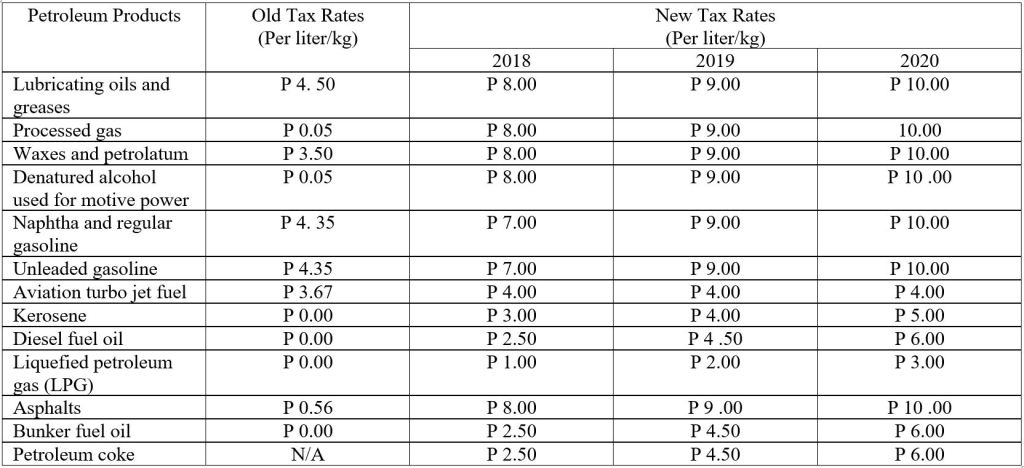

Excise Tax on Petroleum Products

R.A. No. 10963 increases the tax rates on petroleum products in three {3) tranches beginning January 1, 2018 to January 1, 2020, as follows:

As seen in the table above, diesel fuel oil, and liquefied petroleum gas (LPG) are not subjected to excise taxes before TRAIN. Currently, they are being taxed at P6.00 per liter and P3.00 per liter, respectively. Since Filipinos rely on oil to conduct most of their activities like in transportation and food consumption, consumers are affected by the additional imposition of excise taxes because it has increased market prices.

Excise Tax on Sweetened Beverages

Beverages Covered:

- Sweetened Juice Drinks

- Energy & Sports Drinks

- Cereal & Grain Beverages

- Tea & Coffee

- All Carbonated Beverages

- Sweetened Tea

- Flavored Water

- Powdered Drinks not classified as Milk, Juice

- Other non-alcoholic beverages that contain added sugar

Another addition to items subjected to excise taxes are beverages such as: sweetened juice drinks, sweetened tea, carbonated beverages, energy & sports drinks, other non-alcoholic beverages that contain added sugar, etc. Before TRAIN was implemented, these beverages are not taxable. However, upon its implementation, there is now a tax of P 6.00 per liter per volume capacity on sweetened beverages using purely caloric sweeteners, or a mix of caloric sweeteners, and P12.00 per liter per volume capacity on sweetened beverages using purely high fructose corn syrup (HFCS) or in combination with any caloric or non-caloric sweetener. On the other hand, sweetened beverages using coconut sap sugar and purely steviol glycosides are exempt from excise tax. The purpose why legislators decided to tax these items is because it is taken as a health measure primarily to decrease or eliminate as much as possible the consumption of sugary drinks of Filipinos. In a study published in the Journal of the ASEAN Federation of Endocrine Societies, the prevalence of diabetes in the country is about 7.1% in adults from ages 20-79 years old in 2019.

Meanwhile, milk products including plain milk, infant formula milk, powdered milk, meal replacement & medically indicated beverages, ground coffee, instant soluble coffee, pre-packed powdered coffee product, 100% natural vegetable juices, and 100% natural fruit juices are not included in the list of beverages subject to excise tax.

Excise Tax on Cigarettes

RA 10963 increases the excise tax rates on cigarettes packed by hand and packed by machine, as follows:

Old tax rates:

New tax rates:

Tobacco products were also one of the commodities affected by the TRAIN law. Excise taxes per pack of tobacco imposed under the classification ‘Cigarettes packed by machine’, was increased from P30.00 to P32.50 on January 1, 2018. On January 1, 2022, the rate has gradually increased to P40.00, and eventually, come January 1, 2024, the excise tax rate is to be increased by 4% every year thereafter.

The Department of Health in their Global Audit Tobacco Survey in 2015 recorded 15.9 million adults or 22.7% of the total population of Filipinos currently smoke tobacco daily. At the same time, research conducted by a non-government organization Tobacco-Free Kids showed that about 110,000 Filipinos dies from tobacco-related diseases each year. The use of tobacco and its harmful effects prove to be detrimental, not only to its users, but also for other people who are unintentionally affected by this habit.

How TRAIN Law affected our Economy and the lives of Filipinos

TRAIN law changed a lot of things. Its important provision was the amendment of the Income and Excise Tax. We mentioned these two salient points of the law because it greatly affected the financial aspect of each Filipino.

The new income Tax relieved majority of the population in paying its Income taxes. However, the fact that we also pay our taxes indirectly, and the Government collects it thru the value added tax or excise tax should be acknowledged. It means that even if we don’t pay income taxes, some goods and services would become more expensive brought by the effects of the new excise tax.

Transportation is vital to all Filipinos, we use cars to go to work or school, we use ships to transfer goods and services into and out of these islands, and we use planes to reach international destinations at speed. All these modes of transportation rely on one thing, and that’s petrol. In October 2018 inflation hit 6.7%, moving further away from the Bangko Sentral ng Pilipinas’ target range of 2-4% for 2018. Although the causes include world oil prices or other forces, it shows that the rise in inflation was partly caused by TRAIN.

Due to drastic surge of inflation to record high, it was evident that TRAIN aggravated the difficulties of millions of lower-income Filipino households that include fisherfolks, farmers and other poor sectors of the society. This impact was primarily due to high excise taxes levied on oil and petroleum products. This has exacerbated poverty in Philippines by 0.26 percentage point.

In December 2019 prior to the pandemic, the inflation was brought down to 2.5%. It means that prices of commodities became more stable and more accessible for everyone. From 2017 to 2019 the poverty rate went down from 23.1% to 16.7%. The drop in poverty statistics was brought by the improvement of the middle class.

Conclusion

To determine whether the effectivity of any tax reform is always an ever-changing and shifting subject. There are several factors that can affect how our financial structure progresses from time to time. Based on the data we have gathered, TRAIN Law on its early days had a negative impact to financial system especially the rising of prices of commodities. While the lower class and some of the middle class safeguarded by the tax exemption, TRAIN Law failed alleviate the situation of the poorest of the poor. TRAIN Law failed to address income inequality, although it managed to aid the middle class. Nevertheless, TRAIN law was a scheme by the government to collect tax for their major infrastructure projects. It remains to be unseen whether RA. 10963 did achieve its goals.

General source: Tax Changes You Need to Know under RA 10963